A business analysis of Tesco, including SWOT, PESTLE and Porter’s Five Forces

The world of retail has a number of leading brands and Tesco occupies the pride of place as one of the top retailers. It operates 2,318 stores and employs around 3,26,000 people. Tesco UK has the largest market share and operates under four brands – Extra, Superstore, Metro and Express. Own label products are based on three levels: value, normal and finest. Most of the large Tesco stores also have gas stations whose presence makes it the largest petrol retailer in Britain. This report on Tesco UK is divided into three parts. (Tesco.com)

Part one talks about Tesco’s macro environment and provides a brief overview of competitive environments.

Part two discusses the marketing mix

Part three highlights recommendations.

Part 1:

Macro environment:

2. PESTEL ANALYSIS

The PESTEL analysis looks at the political, economical, social, technological, environment and legal factors in a country, which a company has to take into consideration when conducting business in that country.

2.1 POLITICAL ANALYSIS

During the general election held in May 2010, UK voters delivered a fractured mandate that resulted in the first coalition government since the Second World War. This is not a good sign for the economy because the two parties, Conservatives and Liberal Democrats, who have come together to form the coalition, have different principles and this results in slow decision-making processes.

During 2009-2010, when the Labour government was in power, the government was proactive in tackling low growth. It reduced VAT, which enabled consumers to buy products from retailers such as Tesco at lower prices. The government had undertaken a slew of measures to try to make consumers spend more. Some of the measures taken include interest rate cuts, encouraging banks to lend more to customers etcetera (http://europa.eu ).

2.2 ECONOMIC ANALYSIS

The UK has not fully come out of recession. The increase of VAT to 20 % will be detrimental in the shorter term with fewer consumers spending at retail stores. The data for retail sales has not been positive because the government has mentioned that there will be more job losses in the public sector, which will lead to even further job losses in the private sector. This will dampen whatever recovery the supermarkets saw after the recession (http://www.pwc.co.uk).

2.3 SOCIAL ANALYSIS

The UK population is growing at the rate of 0.6% a year. This growth, along with the inflow of migrants, provides a good number of potential customers for retailers such as Tesco to attract and retain (www.optimumpopulation.org).

Most of the UK’s population tends to have food on the move. The UK out-of home food and beverage market is estimated at £37 billion and has an estimated 228 million daily meal occasions. Even though there are a number of players in this market, such as M&S, Sainsbury, Boots, Subway, Greggs and Pret A Manger, it provides a good opportunity for Tesco to focus on this market and build its share (www.sandwich.org.uk).

Consumers can easily switch to other suppliers. They are rapidly reassessing how they can continue to afford their lifestyle, and are changing where they shop in an effort to survive the credit crisis (www.foodinternational.net).

2.4 TECHNOLOGY ANALYSIS

The UK has always been at the forefront of technological innovations. Recent technological innovations include electronic radio tags, which are in the form of tiny chips incorporated into a product, and these allow staff to keep track of the goods in the store. These chips have reduced shoplifting to a great extent. They also help in tracking the razors from the shelf to the till and out of the door. In the case of a product going through the door without being paid for, an alarm is set off which alerts security. The future use of these tags can be envisioned for a wide range of food and non-food products, which would help staff to know which items are in stock, their whereabouts and their expiry date (news.bbc.co.uk). These tags can be used to find the location of products while they are being transported, through electronic tags attached to lorries, and to keep track of the whole supply chain in a particular area by using them in warehouses. Another envisioned use of the tag is in development of products like ice cream, which can tell if the fridge temperature is not suitable (news.bbc.co.uk).

2.5 ENVIRONMENTAL FACTORS

There is lot of pressure on the UK Government to get tougher with supermarkets to tackle Britain’s growing mountain of food waste. This is because retailers generate 1.6 million tonnes of food waste each year. The supermarkets are taking a slew of measures, such as setting up recycling plants, which bring in additional expenses (http://www.independent.co.uk).

Supermarkets are being urged to create a “low-carbon economy” so as to combat climate change. This involves taking a number of measures to reduce carbon footprint. Huge amounts of greenhouse gases are produced through the burning of fossil fuels for electricity, heating, transportation etc. and these have a drastic impact on the environment, leading to climate change. Carbon footprint is the measure of this impact. A large number of products are brought from different parts of the world, which produces a huge amount of green house gases. Supermarkets have been urged to look at ways to reduce these. Also, carbon Foot printing involves huge costs associated with installing energy efficient equipment and using other sources of energy (www.carbonfootprint.com).

2.6 LEGAL FACTORS

During 2007, supermarkets were accused of price fixing. During its investigation, the Office of Fair Trading unearthed substantial evidence where it found out that prices were fixed by a syndicate that involved certain large supermarkets (Asda, Morrison’s, Safeway, Sainsbury’s and Tesco) and dairy processors (Arla, Dairy Crest, Lactalis McLelland, The Cheese Company (formerly Glanbia Foods Limited) and Wiseman) on the retail prices of some dairy products. These supermarkets and dairy processors were fined individual penalties to a maximum of over £116 million (combined) after they admitted involvement in anti-competitive practices, with severe penalties proposed if this gets repeated (http://www.oft.gov.uk).

Research conducted by a major supermarket showed that, surprisingly, 75% of British consumers look at the “Green theme” when they buy their products. The obvious way to find out how ethical or green a product is is by using information found on the label. But in some cases, label claims may be incorrect and this may result in the keenest of ethical consumers facing tradeoffs. With extra effort needed by the supermarkets to avoid legal complications, this will lead to an additional financial burden on the company (www.economist.com).

Porter’s 5 forces analysis

Competition analysis is carried out using Porter’s 5 forces. The five forces that need to be taken into consideration are competitive rivalry, barriers of entry, threats of substitutes, buyer power and supplier power.

Competitive Rivalry

There is intense competition in the retail market with few major supermarkets and many minor ones. Most of the supermarkets have focused on the food sector but of late they are diversifying into the non-food sector, which intensifies the competition (Rigby and Killgren 2008). Tesco had a market share of 30.5% in 2010 and has been steadily increasing at the expense of other supermarkets (Annual Report 2010). This is a positive trend and it is well ahead of its competitors. The direct competitors for Tesco include Sainsbury’s, Asda and Morrisons, which are closer in the scale and reach as compared to other supermarket chains in the UK retail sector. Each supermarket chain has a few distinctive competitive edges over their rivals. Tesco’s advantage has been its range of stores which are within reachable distance for most of the local communities across UK.

Barriers for entry

The established retail players are in an advantageous position because the barrier to entry in the food retail market is high. This is due to the fact that establishing organised retail requires lot of investment in addition to a major brand building exercise. In most of the cases, brands takes years to develop and under the present conditions, investors would not be in a position to invest huge amount of money with no clear sign of when they could recoup the investment. Also, the current brands are very established in UK and are shaping the buying patterns of the consumers, which means there is little scope for new entrants to establish themselves.

Foreign firms will find it difficult to replicate the success seen in their home country in the UK because of the fact that the food retail sector requires very good local knowledge. This can be judged from the fact that the UK has very few global supermarkets.

Threats of Substitutes

Food is a necessity and therefore, the threat over here is low. With an aim to make shopping a pleasurable experience, the current retail players in the market have been constantly trying to converge and assimilate new innovations with respect to food products or alternative businesses, which make it difficult for it to be substituted.

One threat to be taken into consideration is an internal threat, where one supermarket overlaps with the business of other supermarkets.

Buyer Power

Supermarket chains wield tremendous buyer power because of the fact there are a number of suppliers who are willing to sell the same products to the same supermarket, thereby increasing the options available for the supermarket. Supermarkets differentiate suppliers on aspects like prices, green credentials and consumer loyalty to a particular brand of products. Also, for the consumer, switching power is very low and with the economy going further down, their power will be increased considerably (O’Doherty 2008).

Supplier power

In the case of suppliers of general products, they do not wield any power because the buyer has the option of going to a number of other suppliers. In the case of suppliers that are big branded companies whose products are household names, there seems to exist a mutual dependent relationship because big branded products have a loyal consumer base which will ensure that even if a particular supermarket does not store the brand, the consumer will buy it from a different supermarket. But on the other hand, if the products of big companies do not reach supermarkets, their sales volumes will be affected hugely (Wiggins and Urry 2007).

Part 2:

The marketing mix is mentioned in terms of the four Ps : Product, Price, Place and Promotion. In this part of the paper, all these mixes of marketing are described on the basis of the information of Tesco.

Product:

According to Johnson and Scholes (2003), new products and services demand can be created through changes to the business environment in relation to the budget on the provision establishment. It has been suggested by the Ansoff matrix that the development of new products in the existing market can bring significant consideration towards the development of product strategy by a company’s management. For the purpose of expansion and diversification of the product mix of Tesco, it needs to implement the new product development internally. In relation to the diversification of product nature and its perspective, Tesco should look at it from the portfolio diversity angle. Tesco can introduce new product lines through adopting the changing requirements of the customers.. More attention is required for this, which may lead to additional spending. In addition to major brands, Tesco also stocks own label products in three different categories: value, normal and finest. In addition to food and non-food retailing, many Tesco stores have fuel stations, which not only enhances a customer’s experience but also brings in additional revenue to the company. In fact, Tesco is one of the largest petrol retailers in UK. It also has a presence in other areas of retailing and offers personal financing.

When all is said and done, product differentiation is important to a certain extent, but does not make much of an impact. This is because product differentiation would cost a company a considerable sum of money and the companies tend to pass on this to customers. However, customers will not be willing to pay more for the product. The supermarket cannot keep the product on the shelves for long periods of time because of limited shelf space. Tesco has 40,000 different products vying for space in their stores. It also has around 1,200 organic line products, which is a major draw among its customers (http://www.tesco.com).

Price:

Tesco pitches itself to its customer as the best value retailer. Its marketing department regularly checks competitor’s pricing on 23,000 different products before determining the price it’s going to charge for its customers. Tesco has a national price list through which it maintains its prices consistently across the country. Even in some areas where it is the only supermarket, it does not take advantage of the situation and sticks to its national price list. Its price varies in smaller stores and town centres as the overhead costs are higher and the cost of running the operation per square feet is considerably higher than running operations outside the town centre. The price variations are in the range of 2 – 3 % higher in its smaller stores (www.tesco.com).

Promotion.

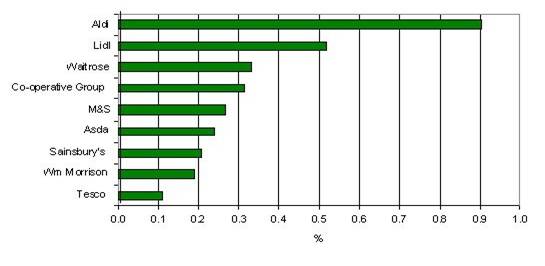

Tesco promotions revolve around its Clubcard scheme and majorly involve direct mailing. This has not been effective of late which can be gauged from the fact that its performance has been slipping. Tesco has been not been spending as much on advertising, which can be understood from the table below

UK: Spending on advertising as % of total sales, 2008, Source: Nielsen Media/Mintel

From the figure, we can understand that Tesco has been spending less on advertising as percentage of total sales even though in monetary terms, it is the second highest spender behind Asda. Tesco needs to spend more on advertising in cinemas, outdoor advertising, TV, press and radio to spread the message of a community-centered supermarket rather than its current perception of a monster out to destroy local communities (Hill, 2008). Tesco has also garnered publicity by carrying out free distribution of samples and this has been a successful strategy so far.

PLACE:

Tesco has a huge distribution network with stores spread across the country. This has made it convenient for it to reach its huge customer base. On the flip side, it has received adverse publicity from the local communities, with people looking at Tesco as the sort of company that is detrimental to its very existence. There have been accusations that whenever Tesco sets up large stores in a community, it takes away the business from small store owners and drives them away from the community, thereby affecting the entire social fabric (Grant, 2007).

Part 3:

Recommendations

| Issues | Recommendations |

| Limited international presence | Tesco must extend its presence to other major markets in the world. The UK market had successful growth over the last couple of decades but this has been cooling over the last few months. Tesco can look at emerging markets like Brazil, India etc. to ensure that it is insulated from the market conditions in UK. Even though it has started building its presence in other major markets like China and the United States, the majority of its revenues come from the UK. Even though it entered the United States in 2007, it has not made any significant progress to date. It also needs to look at other emerging European markets like Romania, which has conditions similar to UK. |

| Inconsistency with Online shopping | There have been number of inconsistencies with Tesco’s e-commerce site . Even though Tesco’s IT system is one of the best in the industry and they have spent a fortune getting it done, it still has problems in processing orders. This has led to numerous complaints from its users. Tesco needs to have the right vision in implementing IT so that it can catch up with Asda (news.zdnet.co.uk). A reliable external consultant has to be appointed who can find out the exact problems plaguing the company and suggest remedial measures. |

| Different store design whose theme is based on the local community | Tesco should look at the option where each store points towards a different shopping experience. This value addition in the form of unique stores offering a different shopping experience can help command higher pricing for Tesco. |

| Intense competition | Tesco can look at the strategy of Backward integration with its suppliers. This way, the company becomes part of the suppliers’ management team and can provide a product of reliable quality and economical price to the consumers |

| Community | Tesco is slowly becoming an icon of globalisation with a paradox of good and bad. There is “Tesco economy” which is providing employment to thousands of people around the globe. Then there are numerous suppliers whose livelihood depends on the way Tesco grows. There are numerous customers who love to shop at Tesco not only because of low prices but also because of the fact that in certain areas where there are local ethnic populations, Tesco sells items that would be very difficult for minorities to find elsewhere. But, the fact is that Tesco is slowly gaining notoriety as a company that destroys small businesses in the neighbourhood. This will make it difficult to gain footholds in certain markets, because of political compulsion. Tesco needs to start engaging the local communities while it plans a store in a neighbourhood. Engaging the local community is a good way to bring about confidence and pass on the message that its presence will not only provides them access to good products at cheap prices, but also increase the employment options available. |

7. Conclusion

With the UK grocery market projected to grow at an annual rate of 2.8 percent, there is a strong possibility that it will reach the magic figure of £150 billion by the end of 2011. In the case of supermarkets like Tesco, the few factors that may slow down its growth would be certain regulatory issues and reduced consumer spending.

With food contributing to the major source of revenue and the demand for food forecast to grow dramatically, Tesco is well positioned to anticipate and meet the increasing focus on fresh, healthy, quality foods. The development of Tesco’s complementary non-food section addresses its customers’ desire to buy a greater range of non-food products along with their weekly grocery shop. The continued development of its convenience stores also takes into account of the faster pace of people’s lifestyles and the trend towards more frequent top-up shopping trips (http://www.tesco.com).

Reference:

Balchin A. (1994) Part-time workers in the multiple retail sector: small change from employment protection legislation?, Employee Relations, Vol. 16 Issue 7, pp.43-57;

Clarke I., Bennison D. and Guy C. (1994) The Dynamics of UK Grocery Retailing at the Local Scale, International Journal of Retail & Distribution Management, Vol. 22 Issue 6, pp.11-20;

Data monitor Report (2003) Food retail industry profile: United Kingdom, January;

Data monitor Report (2003) SWOT Analysis Tesco PLC, July;

Data monitor Report (2003) Company Profile: Tesco PLC Analysis, October;

De Toni A. and Tonchia S. (2003) Strategic planning and firms’ competencies: Traditional approaches and new perspectives, International Journal of Operations & Production Management, Vol. 23 Issue 9, pp.947-976;

Drejer A. (2000) Organisational learning and competence development, The Learning Organization: An International Journal, Vol. 7 Issue 4, pp.206-220;

Finch P. (2004) Supply chain risk management, Supply Chain Management: An International Journal, Vol. 9 Issue 2, pp.183-196;

Flavián C., Haberberg A. and Polo Y. (2002) Food retailing strategies in the European Union. A comparative analysis in the UK and Spain, Journal of Retailing & Consumer Services, Vol. 9 Issue 3, pp.125-138;

Graiser A. and Scott T. (2004) Understanding the Dynamics of the Supermarket Sector, The Secured Lender, Vol. 60 Issue 6, November/December, pp.10-14;

Grant, J (2007), “The green marketing manifesto”, John Wiley and Sons

Johnson G. and Scholes K. (2003) Exploring Corporate Strategy, 6th ed., Prentice Hill: London;

Lindgreen A. and Hingley M. (2003) The impact of food safety and animal welfare policies on supply chain management: The case of the Tesco meat supply chain, British Food Journal, Vol. 105 Issue 6, pp.328-349;

MarketWatch (2004) Company Spotlight: Tesco, Datamonitor, September;

Mintel Report (2004) Food Retailing –UK, Retail Intelligence, Nobember;

Myers H. (2004) Trends in the food retail sector across Europe, European Retail Digest, Spring, Issue 41, pp.1-3;

O’Doherty, J. (2008). ‘Carrefour confident of meeting sales target’, Financial Times, London, 10 January

Rigby, E, and Killgren, L. (2008). ‘Sainsbury buys back sites to fuel non-food growth’, Financial Times, London, 27 March.

Wiggins, J., and Urry, M. (2007). ‘Cadbury benefits from gorilla tactics’, Financial Times, London, 11 December.

http://www.tescoplc.com/plc/about_us/ – Accessed on 13th January at 8 AM

http://ar2010.tescoplc.com/ – Accessed on 13th January at 9 AM

http://www.tesco.com/talkingtesco/productChoice/ – Accessed on 13th January.

http://news.zdnet.co.uk/leader/0,1000002982,39170746,00.htm – accessed on 14th January 2011

http://europa.eu/scadplus/leg/en/s80000.htm – accessed on 14th January 2011

http://www.guardian.co.uk/business/2008/dec/23/economicgrowth-recession – accessed on 14th January 2011

http://www.myfinances.co.uk/news/savings-investments/investments/investment-advice/uk-economy-shrink-over-2-in-2009-$1258580.htm – accessed on 14th January 2011

http://www.optimumpopulation.org/opt.more.ukpoptable.html – accessed on 14th January 2011

www.sandwich.org.uk/docs/taste_experience_07/jeoffrey_young_presentation.ppt – sandwich details accessed on 29th December – accessed on 4th January 2009

http://www.foodinternational.net/articles/news/1509/uk-supermarkets-desperate-to-hold-middle-class-customers.html – accessed on 4th January 2009

http://www.pwc.co.uk/eng/publications/ukeo_video.html