Study on Effects of Interest Rates and Exchange Rates on Consumer Price Index (CPI) in U.K

Number of words: 2851

1.0 Overview of the Study

Evaluating the interest and exchange rates effects on the Consumer Price Index is of crucial significance, especially to the economic policymakers, as it serves as a basis for informed policy decisions at the federal level. Interest rates have a considerable impact on a variety of consumer goods such that higher interest rates deter consumers’ spending on these goods by making them more expensive. On the other hand, exchange rate volatility causes a substantial effect on the domestic price, significantly if it depends solely on importing consumer goods. Therefore, a rise in interest rates and exchange rates is expected to cause a broad category of impacts on the CPI.

This research will explore the concept of exchange rates, interest rates, and the CPI in the context of the U.K. Various empirical inquiries conducted on the interest and exchange rates’ effect on CPI, aiming to establish a clear basis for the formulation of effective economic policies. Interest rates related to the CPI refer to the rate charged for the consumable goods, which predominantly affects the CPI through increased prices when it is high. The exchange rate concerning the CPI is the rate at which consumable goods are exchanged, for instance, when there is international trade; thus, when the goods’ exchange rate is high, there is a substantial effect on the CPI. On the other hand, the CPI acts as a nation’s inflation indicator. When reasonable prices increase, there is an increased expense on the consumers when purchasing these consumable goods.

While efforts to establish a straightforward linear relationship among these variables, policymakers in most cases are averse to reckon with the magnitude of the problem. Therefore, the approach presented in this research is a pervasive one that essentially accounts for the issue. Accordingly, this research will answer the following question: what effect do the interest rates and exchange rates have on the U.K.’s CPI? Previously, it had been hypothesized that high interest rates are associated with increased CPI while the higher exchange rates raise the CPI.

1.1 Research Question

Does the exchange rate and interest impact the CPI in U.K?

1.2 Research Hypothesis

In assessing the impacts of the exchange rates and the interest rates on the consumer price index, the following research hypotheses will guide my study;

H0: No significant effect of the exchange rates on the CPI in the U.K.

H1: Exchange rates affect CPI in the U.K.

H0: The interest rates do not have a significant impact on CPI in the U.K.

H1: Interest rates affect CPI in the U.K

I expect a positive regression coefficient of the exchange rates and interest rates on the CPI from the above-stated hypotheses.

2.0 Literature Review

Several empirical research pieces aimed to assess the impact of the two independent variables, exchange rates and interest rates, on the dependent variable, the CPI.

A study by Goldberg & Campa (2010) tried to quantify the relative significance of the CPI’s responsiveness to the exchange rates. CPI is an index that primarily quantifies the inflation rates in terms of the goods price increase. The study above was done across 21 industrialized countries, which detailed the CPI’s sensitivity to exchange rates. Additionally, the study utilized data from the 21 economies above and found out that the borders’ price movements can drastically influence the CPI. This study implies a significant statistical impact between the exchange rates and the CPI, an inflation index. However, the above research fails to document the effect that both the exchange rates and interest rates have on the CPI. Additionally, our study will use data from the U.K. alone.

The influence that the country’s central bank has in determining the appropriate exchange rates that affect the general price levels is essential for effective monetary policy implementation(Anh et al., 2018). The above research was conducted in the member states of the Association of Southern Asian Nations (ASEAN) in response to several macroeconomic issues using time series data and a vector autoregressive model. The study found out that exchange rate shocks are responsible for the domestic goods price variations. Additionally, the study documents that interest rates’ role in affecting the CPI inflation rates is minimal. However, it is essential to establish whether there is a significant statistical difference between exchange rates and interest rates on the CPI in the U.K. context.

Auer et al. (2021) study the cross-border impact of enormous and impulsive exchange rate appreciation. The research is done at the Swiss border and establishes the exchange rate appreciation for consumers’ spending on domestic and nondurable imported goods. The study found out that any cross-border exchange rate appreciation causes a significant change in domestic prices, with huge impacts on increased retail prices of goods, raising the import expenditure. However, the study fails to account for the significant effects that interest rates have on the CPI. Additionally, it is vital assessing the exchange rates and interest rates’ impact on the CPI in the U.K. context.

Barakat et al. (2015) conducted an empirical study evaluating several macroeconomic variables’ impact on the stock exchange market. The researches primarily aimed to establish the association between the macroeconomic variables and Egypt and Tunisia’s stock market. This study’s variables of interest were CPI, interest and exchange rates, and the money supply. The study’s findings are that there is no causal relationship between these variables and the CPI in Tunisia. Additionally, the study postulates a co-integration relationship of these macroeconomic variables with the stock market. However, in our research, the main emphasis will be on the U.K.’s situation. The aim will be to establish a linear association between exchange and the interest rates with the CPI.

A study by Crawford et al. (2016) shows a detailed CPI movement schedule in the U.K. A similar survey by Klenow & Kryvtsov (2008) depicts a similar CPI trend using 1988-2004 microdata obtained from the U.K. Labor Statistics bureau. The first study uses time-series data whereby there is a significant increase in the CPI with a 0.5 percent margin in the period before seasonal adjustment is made. Additionally, the study postulates an increased CPI value for various consumable goods for two years. However, the studies fail to account for the prime cause of these increased CPI values. Furthermore, since the studies use the data from 2006-2007 and 1988-2004, there are expectations that our research will significantly differ as it will utilize the current CPI data.

Yusuf et al. (2019) research primarily aimed at assessing the exchange rate and interest rates’ impact on economic growth in the Nigerian context using CPI inflation rate as one of the variables. Their study used quarterly time series data spanning 2000-2017. The statistical analysis methods used included the Co-integration and ECM modeling tests. The study establishes a significant exchange rate’s effect and CPI on economic growth. The results obtained from the study imply the exchange rate and the CPI’s causal association. However, in our research, time-series data will be used, relating to the U.K. context, which will help establish the exchange rate and interest rate’s relationship on the CPI. Additionally, our study will explore the interest rate and its effect on the CPI, which is not the case for Yusuf’s Study.

In a study by Di Filippo (2015), a clear indication of the impact of interest rates on banks’ profitability is done in the U.K. context. The research’s main aim established the effect that the low-interest rates have on banking profitability and gives credit to risk assessment. In this study, the approaches utilized include dynamic and static modeling. Additionally, several estimation techniques are used, and the results from the study suggest a significant difference between the low-interest rates and banks’ profitability. The study concludes that reduced bank’s profitability is critical in determining the country’s financial stability. However, the study fails to account for the effects of exchange rates on determining the CPI and its financial stability.

3.0 Methodology

3.1 Variables of the Study

In assessing the impact of interest rates and exchange rates on the CPI in the U.K., the study focuses on macro-economic data on the exchange rate, interest rates, and CPI in the U.K. (1960-2021). In selecting the data, purposive sampling proficiency was utilized. A sample of 26 years’ time-series data for the period 1987-2012 will be obtained for macroeconomic variables used in the study. The study will use the exchange rates and the interest rates as the regressor variables. At the same time, the CPI is the dependent variable. The control variable to be used is the money supply, which regulates the interest rate level. The exchange rate will be measured as value of US Dollar currency in relation to other countries currency, while interest rates is measured as a percentage of borrowed money, and CPI can be measured as the prices of the basket of commodities.

3.2 Functional Form of the Model

The current study adopts a correlation research design to answer the research questions. Ordinary least square (OLS) regression analysis will be used to determine the linkage between interest rates, exchange rates, and CPI. The following regression model will be estimated;

3.3 Research Design

According to Kothari (2004) suggested a causal design, aiding in evaluating one construct’s impact on another. Thus, this research seeks to assess the effect of the exchange rates and interest rates on the CPI in the U.K. and, therefore, measure this relationship’s degree using an econometric construct computed using the OLS technique.

3.4 Ethical Considerations

Ethics is concerned with human behavior and acts as a compass. It is concerned with ensuring integrity when exploiting the processes of data collection and analysis. In relaying the data and information on the variables to be used, this analysis maintains credibility and fairness. According to Cardwell (1999), ethical considerations when doing research include guidance to researchers to ensure the work is conducted in the best interests of the respondents.

3.5 Statistical Data Analysis

This research will use a quantitative solution of analyzing data using summary and inferential statistics. Data will be analyzed using STATA and presented using tables. A regression model will be utilized in assessing the significance of each variable under study. F-test will determine the model’s importance at a 5% level of value.

4.0 Results

This section presents my study results, including the significance of the variables under study and addressing the research hypothesis. The results are analyzed and explained.

4.1 Summarizing Data

In describing the variables, summary statistics will be presented to understand the characteristics of variables. In contrast, inference statistics will be performed to evaluate the individual significance of the variables.

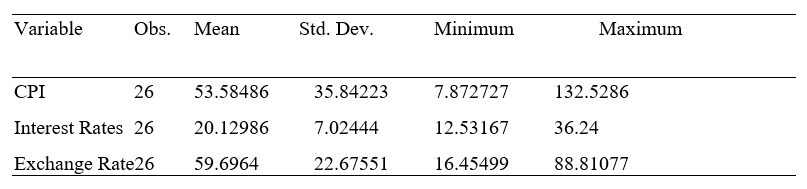

Summary Statistics

The table shows the summary statistics of CPI, interest rates, and exchange rates. The results pointed out that they had averages of 53.585,20.129 and 59.696, respectively. Their respective standard deviations are 35.842,7.024 and 22.676, respectively.

Regression Analysis

Model summary

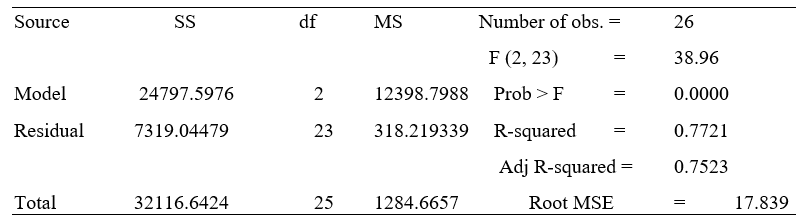

The table above depicts the ANOVA results summarizing the model. The results pointed out that the F (2,23) =38.96, p<0.001; this implies that the overall construct is meaningful at 5%. The results show that the regressor variables are substantial in explaining the CPI in the U.K. The R square is reported as 0.77, implying 77% of variations are defined by the regressor variables.

Coefficients of regression

The table shows coefficients of regression. From the above table, the following model will be used in predicting CPI in the U.K;

From the model above, interest rates had a coefficient of -1.4861, implying that a percentage increase in the interest rates leads to a 1.4861 decrease in the CPI, holding other things constant; this means that interest rates on payment lead to a decreased CPI in the U.K. The slope coefficient implies that interest rates are negatively related to the consumer price index.

Exchange rates had a coefficient of 1.2664, implying that a percentage increase in the exchange rates leads to a 1.2664 increase in the CPI in the U.K., ceteris paribus. The slope coefficient therefore means that exchange rates are positively related to the consumer price index.

The intercept coefficient was reported as 0.8998, implying that holding the exchange rates and the interest constant, the CPI will therefore increase by 0.8998.

4.2 Discussions

Concerning my hypotheses, the interest rates explain CPI in the U.K at 5%, t=-2.91, p=0.008<0.05; thus, H0 is rejected. Also, the exchange rates are meaningful in explaining CPI in the U.K. at 5%, t=8.01, p,0.001; we reject the H0.

Regarding the results obtained above, it was found that both the exchange rates and interest rates are meaningful in explaining CPI in the U.K. CPI was responsive to the exchange rates, implying that exchange rates were significant in explaining CPI. My results are consistent with a study conducted by Goldberg & Campa (2010), who found that exchange rates were statistically significant in explaining CPI. My products also conform to Anh et al. (2018), who found that exchange rates are meaningful in explaining CPI.

Interest rates substantially impacted the CPI in the U. S; these results confirm that Barakat et al. (2015), they found a linear relationship between the exchange and interests on the CPI. My results also confirm the study done by Yusuf et al. (2019), who found that interest rates and exchange rates influence economic growth using CPI as one variable.

5.0 Conclusion

5.1 Summary of Findings

My research aimed to investigate the impacts of the exchange rates and interest rates on the CPI in the U.K using 26 years. The results pointed out that interest rates were substantial in explaining the CPI, even though they hurt the CPI (p<0.001). Also, exchange rates had a significant but positive impact on the CPI in the U.K. The results show that exchange rates strongly impacted the CPI (p<0.001).

5.2 Policy Formulation

From my results above, it is clear that both the interest and exchange rates were substantial in explaining CPI in the U.K. Exchange results had a strong positive relationship with CPI. Therefore the U.K. government should modify the favorable policy regarding the exchange rates. It significantly explains the CPI by maintaining a stable exchange rate through money supply policies.

6.0 References

Anh, V., Quan, L., Phuc, N., Chi, H., & Duc, V. (2018). Exchange Rate Pass-Through in ASEAN Countries: An Application of the SVAR model. Emerging Markets Finance and Trade, 57(1), 21-34. https://doi.org/10.1080/1540496x.2018.1474737

Auer, R., Burstein, A., & Lein, S. (2021). Exchange Rates and Prices: Evidence from the 2015 Swiss Franc Appreciation. American Economic Review, 111(2), 652-686. https://doi.org/10.1257/aer.20181415

Barakat, M., Elgazzar, S., & Hanafy, K. (2015). Impact of Macroeconomic Variables on Stock Markets: Evidence from Emerging Markets. International Journal of Economics and Finance, 8(1), 195. https://doi.org/10.5539/ijef.v8n1p195

Caldwell, C. B. (1999). Understanding research on values in business: A level of analysis framework. Business & Society, 38(3), 326-387.

Crawford, M., Church, J., & Rippy, D. (2016). CPI detailed report. Data for June.

Di Filippo, G. (2015). Dynamic Model Averaging and CPI Inflation Forecasts: A Comparison between the Euro Area and the United States. Journal of Forecasting, 34(8), 619-648. https://doi.org/10.1002/for.2350

Goldberg, L., & Campa, J. (2010). The Sensitivity of the CPI to Exchange Rates: Distribution Margins, Imported Inputs, and Trade Exposure. Review of Economics and Statistics, 92(2), 392-407. https://doi.org/10.1162/rest.2010.11459

Kenneth, G. E. (2021). Statistical Application of Regression techniques in Modeling Road Accidents in Edo State, Nigeria. Sch J Phys Math Stat, 1, 14-18.

Klenow, P., & Kryvtsov, O. (2008). State-Dependent or Time-Dependent Pricing: Does It Matter for Recent U.K. Inflation? Quarterly Journal of Economics, 123(3), 863-904. https://doi.org/10.1162/qjec.2008.123.3.863

Kothari, C. (2004). Research methodology: methods & techniques, (2nd ed.). New age International Publishers, New Delhi, India.

Yusuf, W. A., Isik, A., & Salisu, N. I. (2019). Relative effects of exchange rate and interest rate on Nigeria’s economic growth. Journal of Applied Economics and Business, 7(2), 28-37.