Essay on Bluesky Ltd

Number of words: 2534

A: Advantages and disadvantages of three investment appraisal methods

Advantages of Net Present Value (NPV)

Time value of money: the principal advantage of utilizing NPV is that the time value of money takes into consideration the element of the time value of money. This concept implies a “dollar today is worth more a dollar tomorrow owing to its earning capacity (Kengatharan, 2016, p.15).” Thus, NPV considered an investment’s discounted net cash flows to evaluate its viability. Decision making: NPV facilitates the decision-making process of organizations and aids in identifying whether a particular project yields profits or losses.

Disadvantages of NPV

The method cannot be utilized to compare investments of different sizes: Net Present Value is an absolute figure and not a percentage. As a result, the NPV for more substantial investments would inevitably be higher than smaller size investments. Returns for smaller investments may be higher even though the NPV is lower compared to larger investments with higher NPV (Kengatharan, 2016, pp.16-38). There are no established guidelines of computing IRR: the overall calculation of NPV rests on using the IPP to discount the future cash flows to its present value. However, there is no guideline on how the IRR is determined. The company chooses an IRR, which may compromise the accuracy of NPV. Hidden costs: NPV considers only cash outflows and inflows for a given project and thus does not take into account other hidden costs, preliminary expenses associated with a given project, or sunk costs (Andor, Mohanty, and Toth, 2015, pp.148-172). Thus, the investment’s profitability may not be accurate.

Advantages of IRR

Easy to apply and understand: it is a simple measure to compute and offers easier means of comparing the worth of different investments. Determines the time value of money: IRR is evaluated by computing the discount rate by which the PV of future cash flows matches the required capital investment (Imegi and Nwokoye, 2015, pp.166-170). As a result, the benefit is that cash flow timing in the coming years is considered, and all cash flows are allocated equivalent weight using the time value of money.

Disadvantages

Ignores future costs: IRR does not take into account future costs, which may affect income but considered only the forecasted cash flows generated by a capital injection. Ignores investment size: when comparing investments, IRR overlooks investment size. This is a significant problem as different projects require a considerably different amount of capital expenditure, but the smaller investment return a higher IRR (Imegi and Nwokoye, 2015, pp.170-175). Ignores reinvestment rate: the method enables individuals to compute the value of future money. However, it assumes such cash flows can be reinvested using similar IRR, which is not realistic as such investments that yield such a return are considerably limited.

Advantages of the payback method

Practical in case of uncertainty: companies that have rapid technological changes or uncertainties can benefit from this method as uncertainties make it challenging to forecast future cash inflows. Therefore, undertaking investments with short payback period assist in minimizing the likelihood of loss through obsolescence. Preference for liquidity: other capital budgeting techniques fail to reveal the project’s payback period (Gupta, 2017, p.45). Regularly lower-risk investments have a lower payback period, and such information is essential for smaller businesses with limited capacity as they need to recover their costs quickly to reinvest in other opportunities. Easy to apply and understand: the payback period requires few inputs and is comparatively simpler to compute compared to other capital method techniques (Gupta, 2017, p.45). The only requirements are the project’s annual cash flows and initial cost.

Disadvantages

Ignores profitability: investments with shorter payback periods do not guarantee returns. Cash flows may reduce after the payback period or stop at the payback period. Thus, the investment becomes unviable after the payback period. Overlooks time value of money: time value of money is a vital business concept, and the payback period fails to consider its application, thereby misrepresenting the real value of the cash flows (Imegi and Nwokoye, 2015, pp.175-180). Not realistic: it is a simple method and fails to take into account ordinary business scenarios. Typically, capital investments are not one-time projects and required further investments in the future. Also, such investments have asymmetrical cash inflows.

NPV, IRR and Payback of projects

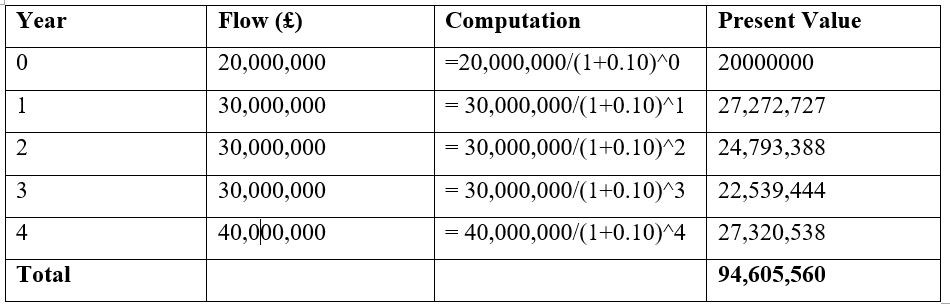

Project 1: Recycling Plant

NPV = (Cash flows)/(1+r) i

i- Initial Investment

Cash flows= Cash flows in the time period

r = Discount rate

i = time period

Initial capital outlay: 40,000,000

Cash inflows:

NPV = 94,605,560-40,000,000

= 54,605,560

Payback period

Payback = 3 years.

IRR

Suppose an IRR of 6.7% and NPV =0:

0 = 20,000,000/ (1+0.067) ^0 + 30,000,000/ (1+0.067) ^1 + 30,000,000/ (1+0.067) ^2 + 30,000,000/ (1+0.067) ^3 + 20,000,000/ (1+0.067) ^4 -130,000,000

= 23,462

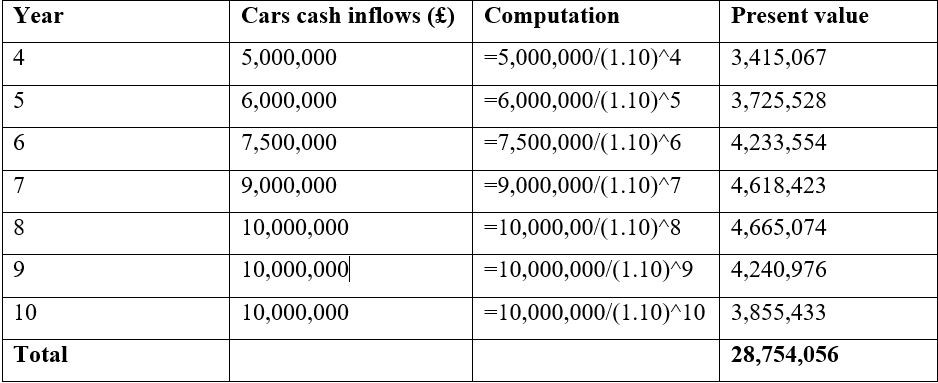

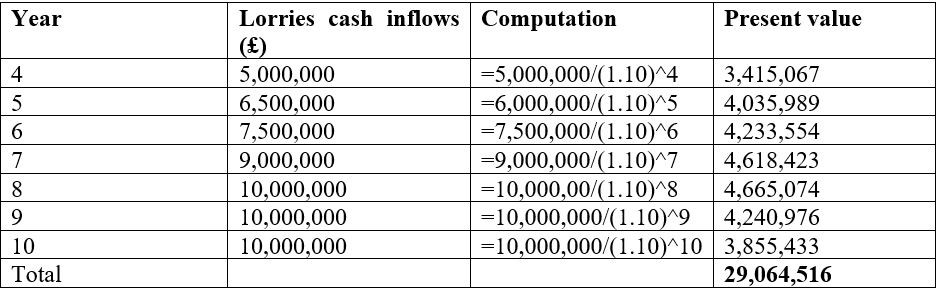

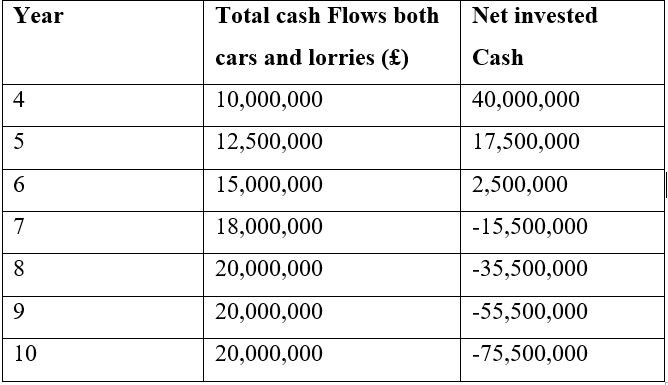

Project 2: Public Toll Road

Cash outlay: 50,000,000

Cash inflows:

Car = cash inflow * £10 * 50%

Lorry = cash inflow * £20 * 50%

Total present values of cash flows for both cars and lorries = 57,818,572

NPV = 57,818,572 – 50,000,000

= 7,818,572

Payback period

Initial outlay: 50,000,000

Payback period = 6 years

IRR

Suppose an IRR of 12.3% and NPV 0

0 = 20,000,000/ (1+0.123) ^0 + 30,000,000/ (1+0.123) ^1 + 30,000,000/ (1+0.123) ^2 + 30,000,000/ (1+0.123) ^3 + 20,000,000/ (1+0.123) ^4 -50,000,000

= 27,372

Recommendation: the company should pursue project 1 as it has a higher NPV and a shorter payback period compared to project 2, even though IFF for project 2 is higher. A higher NPV is more favourable than lower NPV, while a shorter payback period implies that the company will take less time to recover the initial investment costs and thus start making profits. IRR assumes the reinvestment of any cash flows can be reinvested with the IRR.

B: Factors should be taking into consideration before making an investment decision

Funds availability: when making an investment decision, it is crucial to take into account funds availability. Usually, long-term projects require substantial amounts of cash to meet costs like growth in working capital, cost of equipment, and future costs (Imegi and Nwokoye, 2015, pp.181-184). When funds are available, companies can invest in long-term projects, but minimal funds can put the company in financial distress. Funds availability also entails the ability of the company to acquire loans for financing. Larger companies have sufficient collateral to acquire substantial loans than small and medium businesses. Thus, all companies must evaluate whether they have the capacity to secure sufficient funds to undertake an investment.

Expected returns and cash inflows: these are the anticipated growth in profits and other benefits. Companies make investment decisions to increase their long-term financial profitability. Returns are made when there is a decrease in operating costs. Companies should prioritize investments with higher returns and sustainable profits, as these are long-term investments (Imegi and Nwokoye, 2015, pp.185-188). Also, it is essential to consider how much cash inflows the investment will yield. Low cash inflows may suggest a longer time to recover initial investment than higher cash inflows.

Government regulations: companies should consider relevant government policies and requirements. The management must establish licenses needed and payments required in a given investment. For instance, if they anticipate setting up a new plant in a given location, they must observe local laws as some laws may forbid certain plans or facilities.

Risks: most long-term investments are highly risky due to the amount of cash involved. Uncertainties in business operations must be considered. Such risks can either be financial, operational, market, and technological (Chittenden and Derregia, 2015, pp.225-226). Financial risks can be lower returns, which cannot cover operational expenses or lack of loans to sustain cash flow. Operational risks may involve unfavourable weather conditions. Market risks involve sales decrease, emergence of competitors, low demand, changes in interest rates, and exchange rate fluctuations. Changes in technology also pose risks, and management should assess the productive efficiencies of new facilities or equipment (Chittenden and Derregia, 2015, pp.227-230). To deal with risks, investors must consider investment diversification as investments in unique sectors is highly risky compared to across diverse asset classes.

Payback period: companies must consider the time the investment will take to generate profits. More extended payback periods may put the company in financial distress as more funds are channelled into the investment (Chittenden and Derregia, 2015, pp.231-236). If companies require a capital increase in a shorter period, long-term investments may not be viable.

C: Value of Sand Ltd.

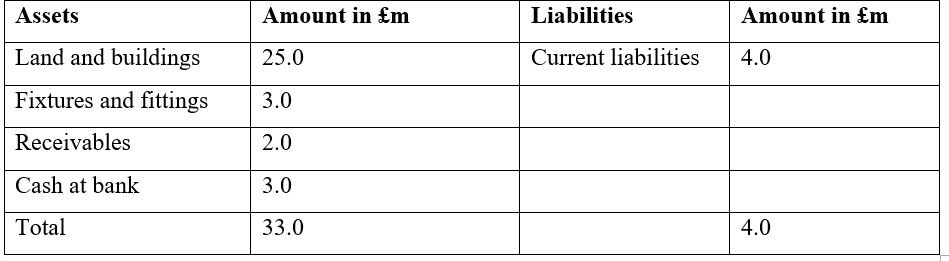

(i). Net asset method (NAV)

NAV = value of assets – value of liabilities

NAV = £29 million.

P/E ratio method

= offer amount/post-tax profits

= £29/ (£10.9-1.2)

P/E ratio = 3.0 which is below current industry average.

The dividend growth model

To determine the value of equity under this method, we apply the formula below:

P =D1/(k-g) where p is fair value price per equity share, D expected dividend, g is the growth rate, and k required rate of return (Maio and Santa-Clara, 2015, p.33).

P = (10*102%)/ (13%-2%)

Value of equity = £92.73

D: Advantages and disadvantages of each of the valuation methods

Net asset method

Its advantages include the method assists as a rationale of evaluation in a schemer of a merger by evaluating the asset backing. Besides, it is useful is valuing property investment companies (Olbrich, Quill, and Rapp, 2015, pp.1-43). The disadvantages are it disregards certain non-balance sheet assets like a qualified workforce. Also, it is challenging in establishing the asset values to utilize since values of particular assets vary considerably based on whether it is valued on a break-up or going concern basis (Maio and Santa-Clara, 2015, pp.34-40). For instance, assets can be valued using realizable, replacement, or historical basis, and accuracy is determined by which method is selected.

P/E Ratio method

The advantage of this method is that the value can be directly associated with other companies trading in the same sector. P/E ratio aids in assessing the company’s risk extent, thus a measure of forecasted future earnings strength (Maio and Santa-Clara, 2015, p.42). Besides, it takes into consideration the company’s profitability, generated from assets as well as investment made within the business. However, this method is not suitable for companies with low profits and a higher value statement of financial position. It may be challenging to use the P/E ratio of quoted companies to value unquoted companies as finding a quoted company with an equivalent range of operations is hard as they are usually diversified (Maio and Santa-Clara, 2015, pp.43-50). In addition, both quoted and unquoted companies have different capital structures.

The dividend growth model

This method is simple to use and understand, as its formula elements are easy to determine. The dividend growth model is suitable for valuing non-controlling interest and also effective in valuing property investment businesses (Plenborg and Pimentel, 2016, pp.55-64). However, it does not consider different shareholder’s expectations. Whereas some are motivated by dividends, others prefer future capital growth on shares (Maio and Santa-Clara, 2015, pp.51-60). Also, the model assumes constant growth, which is not the case in most companies.

In this case, I would advise BlueSky to take an initial offer of £27 million based on the net asset method. The reason being getting a cash offer is certain than stock offers. Stocks may fluctuate in the season hence undervaluing the business and lowering dividends growth.

E: Relative benefits of a cash offer, and a share-for-share exchange for BlueSky Ltd

When BlueSky Ltd is acquired on a cash offer, the amount the investor is going to pay is certain. Thus, this method is less risky for both parties than share-for-share exchange as cash does not fluctuate compared to stocks (Malmendier, Opp, and Saidi, 2016, pp.92-95). For instance, if you purchase another entity using shares and share price rises considerably, it implies you paid more in the acquisition than you would have paid in cash. Therefore, using the cash offer option provides the benefit of guaranteed cash over changing share prices. The cash offer also prevents your company’s ownership dilution. Using your company’s shares to finance another company’s acquisition means its shareholders will become partial owners of your company (Malmendier, Opp, and Saidi, 2016, pp.96-106). As a result, they will have a vote in shareholder decisions and entitled to company profits. A cash offer enables an individual to preserve the current ownership status of the company.

Share-for-share exchanges can be used when the company does not have a large number of shareholders, like BlueSky Ltd, as the stock transaction process would be simpler. Also, these share transactions qualify for tax incentives in the form of tax-free reorganization. Some countries impose taxes on the sale of assets, but share-for-share transaction evades such taxes (Rahman and Lambkin, 2015, pp.24-35). The purchasing entity does not need to bother with costly retitles of individual asset or revaluations as the method simply entail share ownership transfer.

Both cash offer and share-for-share methods have their benefits to each party in the acquisition. However, I would recommend BlueSky to adopt the cash offer option as cash is guaranteed. In addition, they do not want to transfer full ownership of the company to other shareholders. In this scenario, as many shareholders are approaching the retirement age, it would be beneficial for them to accept a cash offer for the purpose of planning their retirement.

References

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of Central and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Chittenden, F. and Derregia, M., 2015. Uncertainty, irreversibility and the use of ‘rules of thumb’in capital budgeting. The British Accounting Review, 47(3), pp.225-236.

Gupta, D., 2017. Capital budgeting decisions and the firm’s size. International Journal of Economic Behavior and Organization, 4(6), p.45.

Imegi, J.C. and Nwokoye, G.A., 2015. The Effectiveness of capital budgeting techniques in evaluating projects’ profitability. African Research Review, 9(2), pp.166-188.

Kengatharan, L., 2016. Capital budgeting theory and practice: a review and agenda for future research. Applied Economics and Finance, 3(2), pp.15-38.

Maio, P. and Santa-Clara, P., 2015. Dividend yields, dividend growth, and return predictability in the cross section of stocks. Journal of Financial and Quantitative Analysis, 50(1-2), pp.33-60.

Malmendier, U., Opp, M.M. and Saidi, F., 2016. Target revaluation after failed takeover attempts: Cash versus stock. Journal of Financial Economics, 119(1), pp.92-106.

Olbrich, M., Quill, T. and Rapp, D.J., 2015. Business valuation inspired by the Austrian school. Journal of Business Valuation and Economic Loss Analysis, 10(1), pp.1-43.

Plenborg, T. and Pimentel, R.C., 2016. Best practices in applying multiples for valuation purposes. The Journal of Private Equity, 19(3), pp.55-64.

Rahman, M. and Lambkin, M., 2015. Creating or destroying value through mergers and acquisitions: A marketing perspective. Industrial Marketing Management, 46, pp.24-35.