Essay on the Process of Digital Transformation in Financial Services

Number of words: 5148

Today, digital business transformation is one of the most important agendas in every aspect of business (Chanias, et al., 2019). Consulting firms, publications, and many other firms have ideas on how digital revolution will change the prospect of businesses, particularly the financial service firms. Digital transformation refers to the reflective effect of utilisation of digital technologies on business procedures and models. However, although most people agree with the idea of digital technologies on financial services, often there is a disagreement on how the idea should be best addressed. The question remains how financial firms can meet financial challenges and grab the opportunities presented by digital transformation. Also, there are concerns on how financial firms can establish methods and tools required to evolve their businesses to become digitally transformed. This paper aims to answer the questions on how business can become digitally transformed by providing an approach that can help banking and financial services organisations to transform digitally while at the same time increasing stability and profitability. Generally, for banking and financial firms to become transformed digitally, they must take advantage of the increasing availability of data and real-time information, make use of machine learning, especially artificial intelligence (AI), to increase organisational intelligence, and create a business model that is more inclusive and interconnecting (Abdulquadri, et al., 2021). Additionally, the firms should come up with interventions that add value to the whole economic system instead of playing a zero-sum game. Additionally, the financial firms must earn and trade on trust central to the overall stability of financial systems entirely through modern technologies.

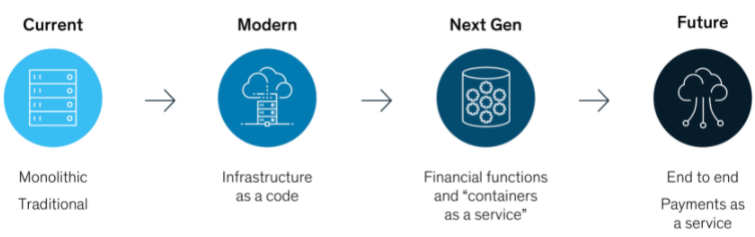

Companies that employ such technologies could probably advance into digitalised financial services institutions, the synapses bank. Synapse banking is a banking service platform that enables banking firms to launch their individual branded financial services easily within the shortest time (Abdulquadri et al., 2021). Financial services institutions which use digital technologies to search for new approaches to adding value are more likely to become more stable and profitable. Digital transformation cab, however, is challenging, and most organisations that anticipate transforming need considerable forecasting and planning. The firms need to shed off old habits, embrace new cultural values, equip their workforce with current skills, and advance their way of making decisions. The traditional business banking model and the majority of financial services used by most companies today were designed and developed based on both tangible and intangible leverages (Chanias, et al., 2019). The leverages have increasingly become unbearable, and thus a new kind of lightness is required to change the financial services industry and become resilient to face the many challenges brought by the anticipated digital transformation in financial technologies as financial systems are being changed through the innovation of new technologies.

Digital Transformation in Payments

The fundamental functions played by financial systems globally have been potentially disrupted. The disruption has been brought by digital innovations and technological changes across various fields, resulting in a new state of unpredictable future. The payment sector is probably the most vulnerable entry point for new FinTech challengers. FinTech technologies comprise various technological innovations extending to the development of cryptocurrencies and the establishment of new rails for clearing and settling transactions and leaving any potential role for customary financial intermediaries such as Central Banks. Online transactions are performed in real-time, and almost no costs are incurred. Digital payment systems are frictionless, transparent, and timeless, creating new revenue opportunities and the advanced roles of data miners and controllers (Dermine, 2017).

Payments Going Paperless

Cash forms the foundation through which people think and understand the nature and main function of financial systems globally (Gomber, et al., 2018). This is, however, an old notion since some Emperors have initiated coning of some forms of money with acceptance by a legal power to clear the transaction regulating the bartering options and increasingly reducing costs and frictions related to deals in the form of cash. Cash has therefore been progressively dematerialised and now happens in digital forms as people are allowed to transact using credit cards or settle transactions through wire transfer. Additionally, digital transformation of payment has allowed charging debit cards without banknotes or exchange of coins at hand. The digital forms of money assume a collective perspective of the concept of cash; however, the amount increasingly becomes marginal as the cash becomes banknote, coinless, and completely digital.

In a paperless community, the payment functions provided by global financial institutions are entirely digitally organized through financial mediators such as banks and credit card organisations. Besides, paperless transactions can be provided by information technology systems and limited and worldwide consultants supervising overall financial systems. Central banks also play a key role in the digital global financial function as they act as the clearers of last resort (Karagiannaki, et al., 2017). Also, Central banks set the terms and conditions of trade for many foreign agencies.

Nevertheless, as transactions become more digital, money becomes critically difficult to regulate, increasing the risk of global financial institutions being attacked. Additionally, going paperless increases disintermediation by other FinTech players. These challenges open up a wealth of opportunities to new digital challengers and enlighten banking players as the two perspectives are usually interlinked and fused in the same company. Digitalisation is used to evaluate interventions to avoid compliance requirements and heavy regulations. The risk of attacking global financial systems also creates new opportunities to embrace current technologies for digital money or cryptocurrencies.

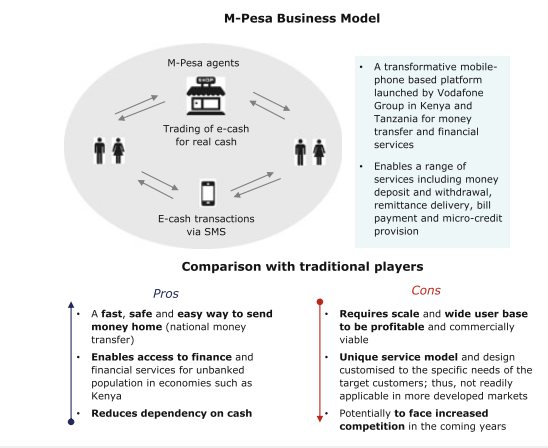

The official payment industry has significantly evolved over time since the introduction of debit cards, credit cards and the increase of e-commerce during the 20th century. The growth of e-payment popularity and the bold strategies currently taken by the Central Bank of Sweden to introduce cryptocurrencies and dematerialise money from paper and coins has greatly contributed to the transformation of financial services. Besides, the Central Bank of India has transformed the economy of paper money into new digital money, reducing the corruption risks and enlightening the black economy. However, full displacement of cheques and cash is still far away in other industrialised countries and under-developed nations like Africa (Gomber. Et al., 2018). Developing nations like Africa are transforming towards digital money through rapid advancement in M-pesa services, for instance, mobile to mobile money transfer, financing and microfinancing services implemented by partnership Vodafone for Safaricom and Vodacom. Although digital money has been rapidly adopted, there are critical challenges that need to be overcome to make the world truly cashless and to eventually provide an opportunity for a radical breakthrough of digital money at local and international levels.

Comparatively, e-transaction carried out in the traditional way still rely on various intermediaries, which are coordinated by large-scale payment networks. Traditional e-payments afford security and acceptance into the system with multiple benefits to consumers and stakeholders. Traditional electronic transactions are convenient, efficient, can be easily tracked, and offer protection to consumers to consumers and stakeholders. A shift to a cashless society will require maintenance of the benefits and overcoming the challenges by the adoption of digital ways of transacting money by all types of businesses and merchants (Karagiannaki, et al., 2017). However, the adoption needs a high level of trust by increasing accessibility, convenience, and protection from cybercrime. Besides, it requires a transformation in the way people culturally think of money. Currently, a number of innovations have emerged which are powerful accelerators towards a truly cashless community. Such innovations include but are not limited to the establishment of mobile wallets, provision of integrated billing services or mobile-based merchant payment options.

Figure 1.0 Payment in a Paperless community

(Khanchel, 2019)

Consolidation of Payments Value Chain

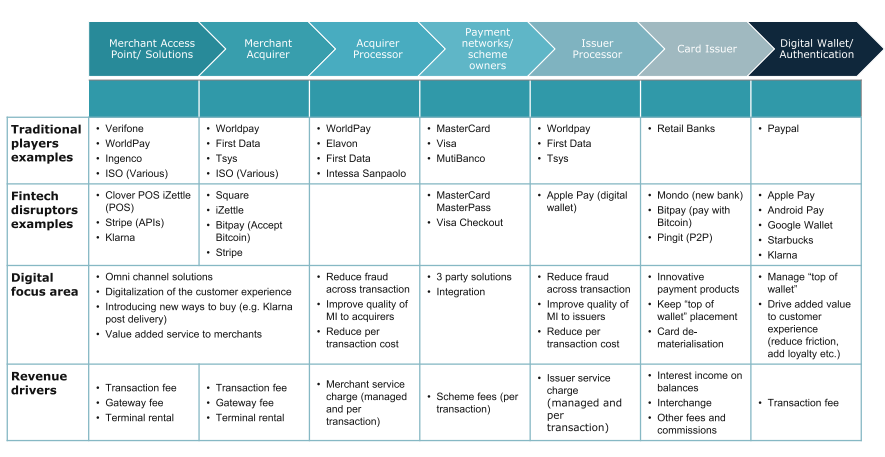

The payment value chain comprises three main components; purchasing, dispensing, and supplying. The value chain begins with the provision of payment solutions to merchants and other businesses, allowing them to perform e-payments. The process starts with the establishment of business by banks and signing up dealers to admit payment cards, making transactions after they are received from the gateway, facilitating authorised requests, and bearing the threat of customer evasion or non-fulfilment of the exchanged goods and services. This process helps banks become more liable for the core relations with merchant which help in the growth of commerce. However, digitisation has disrupted the payment value chain exposing traditional revenues at risk (Li, et al., 2020). The FinTech companies have attacked the traditional players across the value chain offering new opportunities for value-added services. The new technology offers omnichannel solutions and improvement of customer experience by presenting new techniques of purchasing and retailing direct credit lines. Digital technology promises the merchant reduced fraud, reduced transaction costs, and improved quality of information flow to the acquirers. FinTech companies also offer third party solutions for payment networks and have presented innovative payment products and dematerialisation of plastic cards. Ultimately, FinTech companies have introduced a new phase of digital wallet or authentication. They manage the overall wallet and facilitate value-added services to improve customer experience.

Figure 2.0 below represents an analysis of the break-up of the payments value chain whereby there are four drivers to financial services transformation, and that could potentially transform the competitive landscape of payments by attacking the front and back end components of its value chain and systems. The digital players are entering the sector and consequently increasing competition for the benefit of the consumer (Omarini, 2017). Besides, new payment rails are established as an alternative for existing payment systems opening up new technologies for limitless opportunities in data gathering and mining to get better insights of customers and eventually increasing wallet share that the customers spend or invest in their everyday life.

Figure 2.0 Payments Value Chain and Disruptions from Digital Technology

(Omarini, 2017)

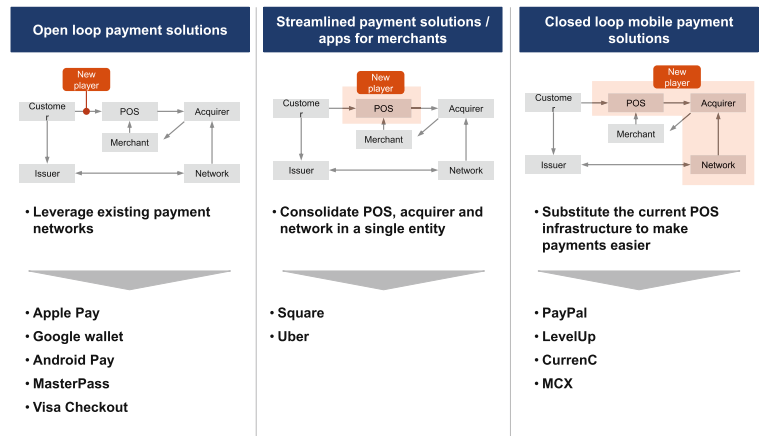

First, discontinuity of payments value chain is driven by entering of intermediaries into the competitive field. In business, payments are significantly driven by technology; thus, new players are inventing the sector through the existing ones, for instance, telecom adjacent to M-Pesa, or the new players are newly established without licensure to operate (Fabian, et al., 2021). The innovators enter the market by offering open-loop payment solutions such as mobile wallets or providing streamlined payment solutions for merchants. Besides, they can also provide closed-loop mobile payments to capture and control some marketplaces.

The new players of the open-loop payments include Apple, Amazon, Google, and FinTech companies like MasterCard and Visa. These companies leverage the existing payment systems as well as improving the services through new technologies such as near field communication and one-click payments. The open-loop competitors directly affect incumbent banks by increasing competition through a default card since many players will push for transactions that settle a single registered card (Gomber. Et al., 2018)). Although, in the open-loop payment solutions, the loop is open to every individual, what matters the most is the flow of information and the ability of the loop manager to read through it.

Figure 3.0 Front-end View of e-payments

(Gomber. Et al., 2018)

The consolidation of digital wallets at various digital payment platforms indicates that many financial service entities will inevitably continue facing risks to lose control over their customer transactions experiences, especially if improved ways of making payments are in real-time, safer, more seamless, and less expensive as devised by new FinTech players. Nevertheless, the more the environment is rich in data, the more it improves capitalisation of current customer relationships and benefits banks if they can capture, store, and manage abundant data (Gomber. Et al., 2018). Therefore, in the future, synapses banks should prepare for future payments by capitalising on much data and providing new intelligence services to customers by use applied analytics and artificial intelligence technology. The new technology can be applied in gaining and solidifying market shares on wallets and promoting more monetary and non-monetary goods and services. Moreover, banks as financial intermediaries should establish sustainable competitiveness by interconnecting with the relevant players of the payment platforms in value addition mechanisms.

The digitalisation of Funding Services

The digital transformation of banking is likely to change funding of the retail and wholesale business. The transformation results in social discontinuities and changes in the way people live as they benefit from the prevailing financial systems leaving behind the most vulnerable. The development of new web-based funding initiatives promises cyber capitalism, an initiative that is open to persons with small coinages and a good wi-fi connection (Fabian et al., 2021). From a wholesale funding perspective, web-based funding initiatives enhance transparency and liquidity, thus creating better funding opportunities for medium and small businesses. However, in retail banking, new funding solutions could be established through the core deposit-taking bank business opening new opportunities for creating new value impacting, impacting joblessness and inequality.

The development and dominance of the capitalism model have been accelerated by investment banks and global financial systems as a result of exacerbating episodes of booms and busts and evolvement of the economy. Traditionally, capital raising was facilitated by certain institutions that grew globally over time, influencing the economic policies of supreme nations. Although the traditional model of funding fulfils the scale and scope of global financial systems, it has significantly contributed to banking instability leading to the new unbearable lightness of increased velocity of investment risks. The traditional approach also poses several challenges which prevent financial systems from fulfilling maximum allocation of scarce capital. However, in an environment where every individual is a dealer, it allows networking and trading directly and easily (Gomber. Et al., 2018). The asset managers shift from being price takers to price makers.

MarketAxess enables asset managers to propose their prices to active persons on the platform. They can access consumer information and infrastructure services. The advantage of the platform is that it provides security and protection for investors and consumers by avoiding any potential conflicts of interest. Tradeweb is a digital funding solution that provides advanced trading solutions for middle-market investors, broker-dealers, and financial advisors. Tradeweb offers a fast and efficient trading approach to the full range of fixed income securities. Besides, it allows access to live offerings, accurate real-time pricing, fast execution, and a deep pool of liquidity. In such a scenario where everyone is a dealer, every user can quote a bid or ask price for all the bonds traded on the system, therefore, leading to increased liquidity, transparency, and efficiency (Saal et al., 2017).

The utilisation of machine learning artificial technology can help in data aggregation and optimise management of unstructured data, hence helping in shaping offerings and channelling strategies for understanding the financial health and personal side of the customer. Machine learning and AI applications can identify the target client and what they could aspire to be in the future (Scardovi, 2017). Additionally, virtual mobile and banking platforms have established new and richer approaches to various interconnecting stakeholders. The platforms also offer stakeholders new use cases and solutions, adding incremental value to the ecosystem. These new technologies in financial and banking services are key arising potentials for future retail banks and the funding function. The new FinTech players, on the basis of trust, can capitalise and have increased control over their customer relations due to advanced and digitalised interactions, which help overcome inertial reservation of consumers to swap from their previous banks (Saal et al., 2017). From this perspective, traditional banks can evolve by acting on the synapses levers to improve customer relations and reduce capital burden as product manufacturers. In this scenario, the traditional banks would not act as intermediaries but rather aggregators of multiple non-financial suppliers to deliver the targeted customer intentions. From a disruptive perspective, new FinTech would compete with the manufacturing side by developing virtual financial systems with an emphasis on client management. The virtual banks would offer comprehensive products through a partnership with different alternative financial service providers ranging from peer-peer lending, payments, and crowdfunding. This would provide a competitive advantage to new FinTech companies.

Revolution in Investment Management

The digital transformation has affected investment management from four perspectives. First, digital transformation allows comprehensive participation of people in global capital markets, leading to cyber capitalism, whereby the capital markets are open to everybody. Digital transformation secondly contributes to the development of a trading battlefield between machines and AI-powered algorithms. Thirdly, digitalisation transforms financial advisory due to the emergence of robots that are increasingly becoming better at that task. Finally, digital transformation has led to the industrialisation of office activities. Markets and societies are also highly advantaged by digitisation; however, new risks result as algorithms tend to give similar results with unclear potential effects partially addressed. According to Scardovi. (2017), successful transformation in investment management relies heavily on the optimal relationship between humans and machines.

Management of Money and Power

Traditionally, the management of wealth was associated with rich people. However, this belief will be soon challenged as management of wealth traditionally offered by various financial firms, including commercial and private banks, broker-dealers, family offices, and insurance companies, are going to be available for every person. The transformation ranges from higher to lower-end consumers based on the investable financial assets. In the future, every individual will play a role in investment management due to a new form of capitalism, including leveraging of information and data, AI and applied analytics, and current forms of digital interconnectedness (Scardovi, 2017). All these digital forms of capitalism have been made available by the use of sophisticated technologies and robots for financial advisory.

The investment management sector has suffered a loss of trust since financial issues related to poor performance remembered by alpha is challenging to attain and ensure with time. Additionally, diversity, the key rationale for value addition in investment management, usually collapse due to poor markets and break down of correlations. The wealth management sector, therefore, experiences cases of fraud and embezzlement of funds and episodes of miss and cross-selling. However, among all these critical issues, loss of trust for the industry is the hardest to recover (Schmitz, et al., 2019). Some authors argue that entering and exiting customers should be charged fixed fee commissions. Nevertheless, the amount of charged commission has been too high and cannot be justified by the extra services offered to customers at the end.

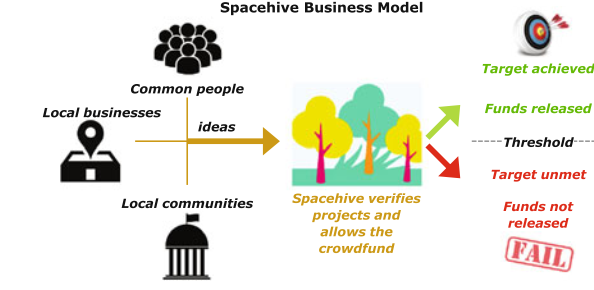

The FinTech challengers in this context have initiated multiple disruptive propositions by delivering automated wealth management services. The challengers offer digitalised investment management services on trading platforms at low costs. Nonetheless, the investment solutions are sophisticated to support ideal portfolio generation and selection of investment strategies through automated generation of recommendations. Automated investment management platforms such as Spacehive creates target offerings focusing on support of local projects. This technology empowers people to have increased, and cost-efficient control of their wealth and their choice of investment and increases access by many people left behind. Digital technology also erodes the core business of private, asset, and wealth managers by offering advanced investment intelligence and high technology services at lower costs than the traditional model of offerings.

Figure 4.0 Spacehive Business model

(Schmitz, et al., 2019)

The Spacehive business model allows for greater visibility for community projects and offers an alternative financing option for the public sector. Also, Spacehive investment technology benefits the community as they become the judges of project impacts and are responsible for the outcome. However, given the unattractive project returns, big-ticket investors are unlikely to participate. Another disadvantage is that the size of financing is limited compared to the nature of the project, and geographical constraints are also experienced.

Multiple FinTech players are increasingly increasing access for the few investors who have been left out by basic banking proposition. The improved mousetrap targets highly earning individuals receiving investment services from private financial entities and financial planners who are increasingly unable to justify the highly charged commission with reduced value propositions. FinTech digital inventors ensure increased control and transparency to the end consumers affording greater prominence of their financial plans and optimised risk/return portfolio. Embracing the new investment technology enables customers to have increased accessibility to new wealth management opportunities (Sebastian, et al., 2020). The digitalised investment technologies increase convenience as online and offline channels are leveraged to increase interconnectedness with customers. Customers have enhanced delivery of financial analysis services in real-time and at a reduced cost nearly zero marginal cost. Moreover, as data becomes increasingly available over the web or through IoT applications, the companies are able to mine updated social and behavioural data, therefore, leading to the delivery of personalised and high profile investment solutions (Saal et al., 2017). The FinTech players improve the wealth dimensions of reach and richness in a number of ways. First, they provide faster and cheaper online investment management tools and robotic services. Secondly, the digital innovators have expanded reach dimensions whereby the underserved or non-served market customers are targeted.

The crowd cube is a crowdfunding website based on equity. It allows entrepreneurs to potentially invest online and raise capital from other people in return for equity. The business model is powered by artificial intelligence technology, which facilitates searching, analysis, and visualisation of the global business investment approaches to identify opportunities for improvement. Crowdfunding is a flexible financing structure that allows the interconnectedness of firms and finance providers.

Transformation in Lending

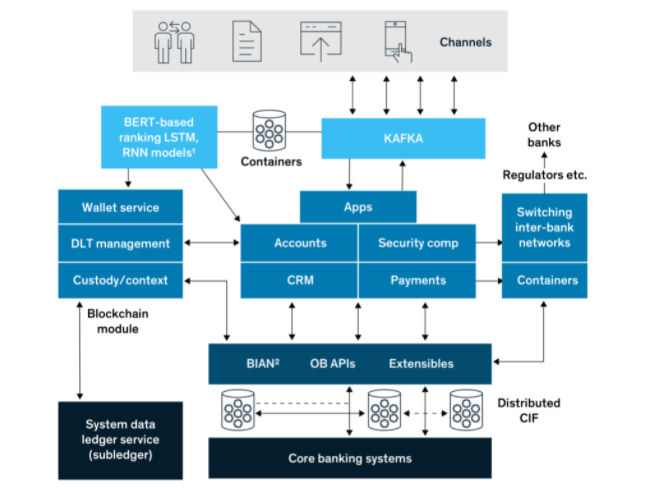

Lending is a core banking function, and digitisation of the lending process is associated with multiple benefits to banking institutions, including improved decision making, better customer experience, and cost-saving. Although the transformation of the lending process could be challenging, it can lead to improved performance. New technologies have opened for innovative payment strategies, and to take full advantage of such new technologies, payment providers must modernise three key components of their legacy technology (Singh & Hess, 2017). Lending firms must modernise their infrastructure and deployments, including data, recording systems, and tokenisation. Second, the middleware ecosystems need to be digitalised, including routing, authorisation, analytics, risks, and instruments. Lastly, the modernisation of front-end channels and execution systems is key and includes the transformation of customer experience, offering evenly distributed point-of-sale solutions, and financial wellness. Nevertheless, these significant transformations are underway in most banking and financial services entities. According to Schmitz, et al. (2019), the payment infrastructure is undergoing significant transformation, as indicated in figure 5.0 below.

Figure 5.0 Digital Transformation of Payment Infrastructure

(Schmitz, et al., 2019)

Advancements in open-source technologies, cloud computing, and decentralisation have ensured flexibility and provision of on-demand services, paving ways for new FinTech technologies such as Square, Adney, and Stripe to interrupt the space. Financing entities have now entered into an era of financial functions as service paradigms. Although it has never been easier to establish flexible and fully robotic systems, with the increasing use of open-source technologies, it is now easier to apply advanced technologies to simplify credit decisions, minimise churn returns, and optimise authorisation rates while reducing declines. In the future, we expect fully computerised and optimised payment as a service for payment functions such as routing, tokenisation, and stand-ins, whereby they are coded as separate functions assembled in a superior manner that provide an excellent customer experience (Tana & Breidbach, 2021). The flexible, modular, and computerised payment systems have facilitated the rapid adoption of cutting-edge technologies such as artificial intelligence, DAG, and blockchain, empowering the next generation of cards and payment technologies.

Internet of things (IoT) has led to increased connectivity and embedment of transactions making the payment card sector vulnerable to disruptions. Although the disruptions are at their early stages, they can lead to significant transformations. Faster adaptation and continuous investment can modify the existing infrastructure, enabling payment providers to devise new approaches for overcoming challenges and ensure the rapid establishment of new products and services. The figure 5.0 below by Tana & Breidbach. (2021) represents the flexible payment architecture that can facilitate the rapid rollout of emerging products and the integration of new services. The architecture would enable blockchain augmentation of the existing banking and financial systems to implement credit cards to reduce the cost of cross-border payments, reduce the general cost, and enhance security.

Figure 5.0: A Bidirectional Representation of Technological Transformers

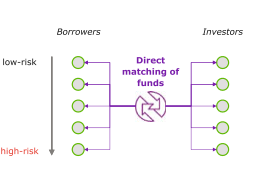

These digital disruptors have contributed to leveraging online data and websites to offer direct matching of funds between savers and borrowers without necessarily having intermediaries’ organisation’s balance sheet. The digital disruptors facilitate peer-to-peer networking, thus ensuring reduced service and funding costs as their cost structure is agile and IT-driven. Besides, the digital disruptors do not need branch networks, compliance to regulations and management of risks and provision of financial advice is done by automated machines, and credit scoring tools are based on AI technology (Tasneem, 2017). The digital disruptors, therefore, are lean, efficient, and effective in buying and selling money. They can assemble their borrowers and lenders on-board and evaluate them in a streamlined way in accordance with predefined procedures of fast, transparent, and democratised processing without leaving any room for personal relationship banking. This funding circle benefit the client on lower funding costs compared to the traditional lending model.

Figure 6.0- The Funding Circle Business Model

(Tasneem, 2017)

In the funding circle business model, the cutting-edge technology is combined with industry resulting in credit scoring models which account for both structured and unstructured data coming from the counterparts. Besides, the model embraces applied analytics to find the perfect match between borrowers and investors based on their computerised risk-return profiles (Tekic & Koroteev, 2019). The intermediation model can serve all credit markets and enhanced choice on your own recommendation. The model implements an enhanced financial system for risky loan borrowers by facilitating easier access to credits. Lastly, the reputation of the lending platforms depends mainly on the quality of disclosure of borrowers’ data to the investors. Although the model is advantageous, it offers limited guarantees on investments and acts only as a marketplace without direct responsibility for the originated loans.

Conclusion

The traditional business models in the banking and financial service entities were previously developed on the basis of leveraging global financial systems. However, due to the innovation of new technologies in the provision of financial services, the financial service industry is faced with a number of challenges that need to be addressed. Financial service institutions that embrace digital technologies experience improved business operations, processes, and models. The institutions also become more stable and profitable. These digital banking and financing technologies can be achieved when companies take advantage of the availability of big data and real-time information. Also, the digitalised technology can be achieved by the use of machine learning or artificial technology to establish more organisational intelligence and increment of interconnectedness. The application of new technologies in the delivery of financial and banking services has led to a tremendous transformation of payment processes by developing digitalised payment approaches (Zachariadis & Ozcan, 2017). Besides, funding services, investment management strategies, and lending services have been greatly impacted by new technologies. Digital disruptors of the traditional banking and financial services approaches have contributed to leveraging of online data and websites to offer direct matching of funds between savers and borrowers without necessarily having intermediaries’ organisation’s balance sheet, hence changing lending services for good. Advancements in open-source technologies, cloud computing, and decentralisation have ensured flexibility and provision of on-demand services. Machine learning and AI applications can identify the target client and what they could aspire to be in the future. Additionally, virtual mobile and banking platforms have established new and richer approaches to various interconnecting stakeholders.

List of References

Abdulquadri, A., Mogaji, E., Kieu, T.A. and Nguyen, N.P., 2021. Digital transformation in financial services provision: A Nigerian perspective to the adoption of chatbot. Journal of Enterprising Communities: People and Places in the Global Economy.

Chania, S., Myers, M.D. and Hess, T., 2019. Digital transformation strategy making in pre-digital organisations: The case of a financial services provider. The Journal of Strategic Information Systems, 28(1), pp.17-33.

Dermine, J., 2017. Digital disruption and bank lending. European Economy, (2), pp.63-76.

Gomber, P., Kauffman, R.J., Parker, C. and Weber, B.W., 2018. On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. Journal of Management Information Systems, 35(1), pp.220-265.

Karagiannaki, A., Vergados, G. and Fouskas, K., 2017. The impact of digital transformation in the financial services industry: Insights from an open innovation initiative in fintech in Greece. In Mediterranean Conference on Information Systems (MCIS). Association for Information Systems.

Chancel, H., 2019. The Impact of Digital Transformation on Banking. International Journal of Trends in Business Administration, (2).

Li, J., Huang, X., Wu, C., Yang, Y., Zhang, D., Bai, X., Li, F. and Sun, Y., 2020, December. How Can Blockchain Shape Digital Transformation: A Scientometric Analysis and Review for Financial Services. In 2020 Management Science Informatization and Economic Innovation Development Conference (MSIEID) (pp. 264-267). IEEE.

Omarini, A., 2017. The digital transformation in banking and the role of FinTechs in the new financial intermediation scenario.

Fabian, N.E., Broekhuizen, T. and Nguyen, D.K., 2021. Digital transformation and financial performance: Do digital specialists unlock the profit potential of new digital business models for SMEs?. In Managing Digital Transformation (pp. 240-258). Routledge.

Saal, M., Starnes, S. and Rehermann, T., 2017. Digital Financial Services.

Scardovi, C., 2017. Transformation in Lending. In Digital Transformation in Financial Services (pp. 127-142). Springer, Cham.

Scardovi, C., 2017. Digital Transformation in Financial Services (Vol. 236). Cham: Springer International Publishing.

Schmitz, M., Dietze, C. and Czarnecki, C., 2019. Enabling digital transformation through robotic process automation at Deutsche Telekom. In Digitalisation Cases (pp. 15-33). Springer, Cham.

Sebastian, I.M., Ross, J.W., Beath, C., Mocker, M., Moloney, K.G. and Fonstad, N.O., 2020. How big old companies navigate digital transformation. In Strategic Information Management (pp. 133-150). Routledge.

Singh, A. and Hess, T., 2017. How chief digital officers promote the digital transformation of their companies. MIS Quarterly Executive, 16(1).

Tana, S. and Breidbach, C., 2021. Institutionalising Digital Transformation through Cryptocurrency Use.

Tasneem, N., 2017. Acceptance of digital transformation in the financial sector of Bangladesh.

Tekic, Z. and Koroteev, D., 2019. From disruptively digital to proudly analogue: A holistic typology of digital transformation strategies. Business Horizons, 62(6), pp.683-693.

Zachariadis, M. and Ozcan, P., 2017. The API economy and digital transformation in financial services: The case of open banking.