Essay on Strategic Financial Management

Number of words: 3596

Executive Summary

The objective of this report is to perform financial and non-financial analyses of e-commerce fashion company Boohoo PLC. The report highlights that despite low profitability in recent years, Boohoo PLC is able to increase its sales. Hence, efficiency in managing the cost of operation is required by Boohoo PLC, an e-commerce fashion retail company. The company has been operating in several countries and facing challenges in its supply chain. However, the company focuses on technological innovation and customer satisfaction through which it aims to achieve sustainability. The company can be considered profitable to invest in due to having higher returns for investors.

1. Introduction

(a) Overview of the company

The selected organisation, Boohoo PLC, has been operating in the fashion retail industry. It has also been identified from the vision and mission statement of the organisation that Boohoo PLC aims to become an e-commerce leader in the fashion industry worldwide by meeting the demand of the customers, people, suppliers and stakeholders. The operation of Boohoo PLC is mainly based on the online market (boohooplc.com, 2021).

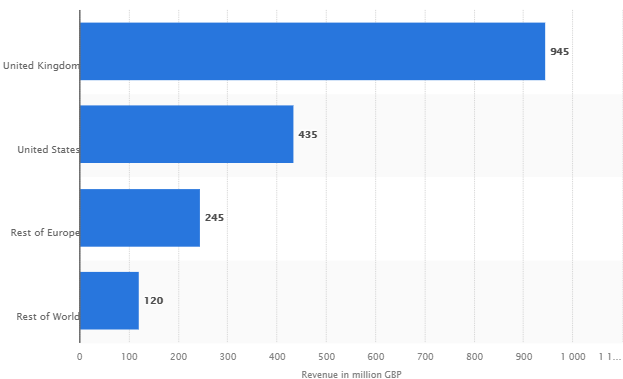

Figure 1: Sales revenue from different regions in 2020-21

(Source: statista.com, 2021)

Furthermore, Boohoo PLC has been operating in more than 100 countries, including the USA, European regions, and the revenue from such regions is depicted in figure 1. Based on the evaluation, the UK (945 million GBP) and the USA (435 million GBP) are the two primary locations where the company has achieved the highest revenue.

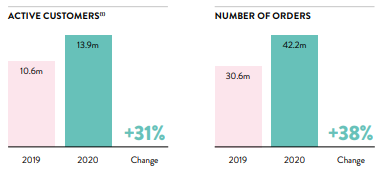

Figure 2: active customers and number of orders in Boohoo PLC

(Source: boohooplc.com, 2021)

The organisation has also developed several brands, including boohoo, boohoo man, little thing, Nasty Gal, Misspap, Karen Millen and Coast. The organisation had 13.9 million active customers in 2020, and the orders from the organisation have also been increased by 38% from 2019 to 2020 (boohooplc.com, 2021).

(b) Purpose of the report

This report will include financial as well as non-financial performance evaluation of the selected organisation Boohoo Public Limited. In order to present such aspects, the relevant accounting ratios will be firstly interpreted in the report. After evaluating the financial performance, the organisation’s strategic decision-making capability will also be analysed by applying important market analysis tools such as PESTLE and SWOT. Lastly, in the conclusion section, the overall findings of the report have been presented.

2. Ratio analysis

(a) Profitability

Gross profit ratio

The evaluation of the profitability ratios helps identify the fact that Boohoo PLC has increased its GP ratio from 52.84% in 2018 to 54.16% in 2021 [refer to appendix 1]. This refers to the fact that before incurring any cost for the other activities other than the cost of the goods, the organisation has sold more goods and is able to increase its gross profit margin resulting in such an increase.

Operating profit ratio

On the other hand, the evaluation of the operating profit ratio helps to determine that after meeting the operational expenses or obligations, the company has generated an operating profit of 7.05% in 2021, which was 7.33% in 2018 (boohooplc.com, 2021). Therefore it can be depicted that the organisation’s operating costs have increased. Therefore, the profitability after meeting the operating costs has decreased in the context of Boohoo Limited.

Net profit ratio

Moreover, the net profit ratio is another important tool of profitability that allows estimating the ability to generate profit after incurring all of the expenses of an organisation. Based on the evaluation of the ratios, it is identified that Boohoo Plc profitability has slightly decreased as it was 5.46% in 2018 and 5.20% in 2021. This indicates that Boohoo Plc was not able to increase its profitability in the last four years. It can be depicted that despite the increase in the revenues, the organisation’s costs increased, resulting in the same position in terms of achieving profits.

Return on invested capital

Lastly, return on the invested capital helps in measuring whether the company is able to generate a return from the capital that has been invested by it for operations; based on the interpretation of the ratio, it is identified that return from the invested capital of the organisation has increased from 3.26% in 2018 to 5.12% in 2021 [refer to appendix 1]. This refers to the fact that more income is now generated from the capital than in previous years. Such an increase in the ROIC also helps to denote that Boohoo PLC is growing and reflects that the business can achieve sustainability (McLaney & Atrill, 2020).

(b) Liquidity

Current ratio

This first liquidity measure that has been incorporated in this report is related to the current ratio. According to Drury (2018), the current ratio is about explaining whether an organisation is able to meet its short term obligation using its short term assets. In the context of Boohoo Plc, it was observable that in the last four years, the organisation is not able to achieve the ideal ratio of 2 times, although the ratio is higher than 1 (boohooplc.com, 2021).

Quick ratio

On the other hand, the use of the quick ratio is also similar to the above measured only in this context; the inventories are excluded when the short term obligations are met. It has been observed that the current ratio has decreased to 1.18 times (boohooplc.com, 2021).

Cash ratio

The evaluation of the cash ratio only considers the ability of the organisation to meet the short term obligation using only cash and cash equivalents. Therefore it is also a great tool to measure the liquidity position. The cash ratio of Boohoo Plc decreased from 1.43 times to 0.97 times. This indicates that in the year 2021, the company is unable to meet the short term expenses using only cash.

Operating cash flow ratio

However, the operating cash flow ratio of the company has dramatically increased from 0.24 times to 0.57 times (boohooplc.com, 2021). This helps in identifying cash inflows from the operating activities. The business’s core activity is profitable; however, the other activities are causing cash outflows (Drury, 2018). An overall analysis of this aspect presents that Boohoo PLC’s cash or liquidity position has deteriorated from 2018 to 2021 [refer to appendix 1].

(c) Efficiency

Inventory turnover ratio

The evaluation of efficiency ratios helps to identify that the inventory turnover ratio has increased from 12 to 14 times in 2021. Therefore, Boohoo Plc is expected to face higher demand, so the turnover ratio is positively affected.

Inventory turnover in days

The same is also observed in the context of inventory turnover in days where the cycle of inventory has decreased from 30 days in 2018 to 26 days in 2021. This means the organisation is taking 26 days to sell its inventories, whereas, in 2018, it was taking 30 days to sell stocks (boohooplc.com, 2021). This has also positively affected the revenue as an increase in the inventory turnover means that inventories are being sold more times, generating more profits.

Payables turnover ratio

The payables turnover has helped explain that the company has increased its payable turnover, which means the company’s efficiency has increased in paying its creditors than the previous years (3.18 times in 2018 and 3.30 times in 2021).

Return on assets

Income from the CGU (Capital generating units) has also increased as Boohoo PLC’s ROA reflects that it was 0.10 times in 2018 and increased to 0.12 in 2021 [refer to appendix 1].

(d) Investor

Earnings per share

Investor ratios are essential for the shareholders and help them to decide whether more investment shall be made in the company or not. Here in the context of Boohoo Limited, the earnings per share have been increased for shareholders indicating that the company profit-generating capacity has increased. The EPS of Boohoo PLC in 2018 was 3 pence, and in 2021 it increased to 7.25 pence per share.

Return on equities

Besides, it is also observable that returns from equities have also increased as it has hiked from 16% in 2018 to 19% in 2021 (boohooplc.com, 2021). The investors are likely to be getting paid more than the previous years, and hence it is profitable for the investors.

Price-Earnings ratio

On the other hand, the PE ratio depicts the price that the market is willing to pay for the company’s earnings. The Price Earnings ratio has decreased from 90.78 in 2018 to 42.77 in 2021 (boohooplc.com, 2021). This indicates there is uncertainty about the future earnings of the company.

Debt to equities ratio

Lastly, the debt to equity ratio is about estimating whether the company is able to meet the liability compared to its equities. Thus, with the help of the debt to equity ratio, the analysts can interpret the degree of leverage of the organisational operations. Boohoo Plc. is found to be having low debts compared to equities as it was decreased from 2018 to 2021, and the share of debt in the capital structure is very low as it is lower than 1 (0.04 times in 2021, and 0.05 times in 2018). Hence, most of the operation is leveraged by equities (Dyson, 2020). The result depicts that risks in this company are very low [refer to appendix 1].

3. PESTLE Analysis

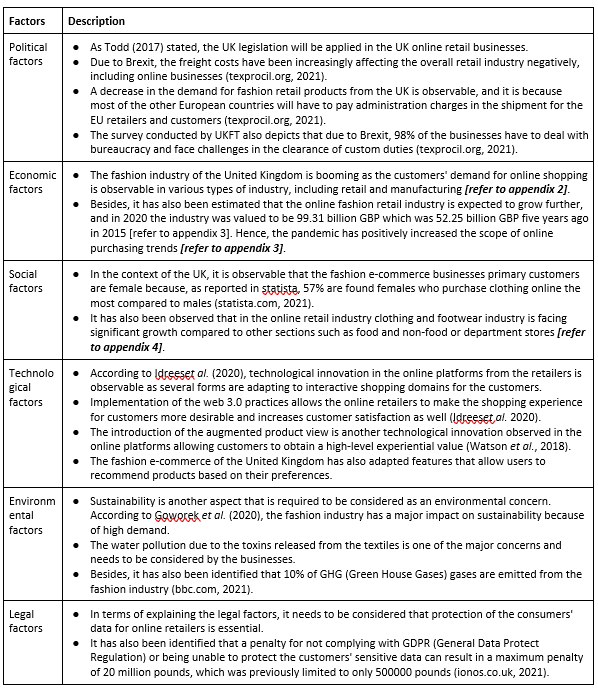

Table 1: PESTLE analysis of the retail industry of United Kingdom

The above table represents the PESTLE analysis, and it has been developed in the fashion e-commerce retail industry. Interpretation of the table helps in identifying the possible threats and opportunities for an online retail company such as Boohoo PLC. The political factions are expected to affect the online retailer negatively because of the increased rate of administration charges the customers, as well as the retailer, has to pay more although FTA (Free Trade Agreement) policies are implicated. Therefore, assessing the position of Boohoo PLC in this context helps to identify that the company is likely to face low demand when the prices of the products in other countries of the EU are increased due to such costs. Besides the legal and environmental factors is also a possible threat for Boohoo PLC as these can impact the stakeholders of the company effectively and can cause loss of reputation in the market. However, a sustainable approach can be an opportunity for the organisation to develop a good brand image and attract more customers (Jung et al. 2020). The organisation’s sustainability goal to achieve zero carbon footprints is observable in its efforts in reducing material wastes and efficient supply chain management (boohooplc.com, 2021). Interpretation of the social factors helps to denote a positive future for the e-commerce retailers as the fashion industry is expected to grow, and therefore revenues are also expected to be high. The increase in the number of consumers in the e-commerce industry can help businesses such as Boohoo gain customer loyalty and brand awareness in the domestic and international markets. In the above table, the economic factors for this industry and for the select organisation are changing positively, indicating growth for the future. Moreover, the technological innovation by online retailers is also helping to increase customer satisfaction. According to Said (2020), the disconfirmation paradigm refers to customer satisfaction going through two phases; pre-consumption and post-consumption. With the application of technological innovation, the pre-consumption experience of the customers has increased, so they have decided to purchase the products.

4. SWOT Analysis

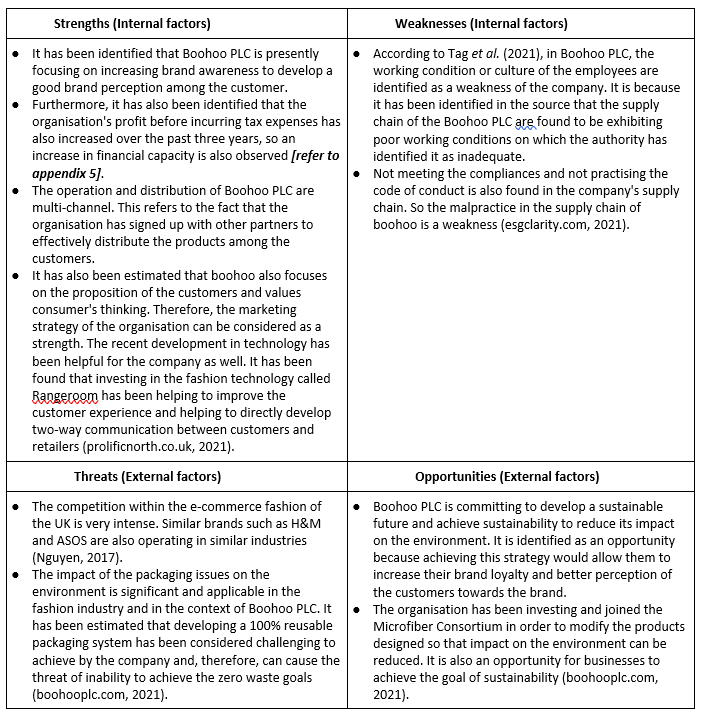

Table 2: SWOT Analysis

Making a complete evaluation of the above-presented SWOT analysis helps to evaluate the strategic decisions undertaken by Boohoo PLC. It also demonstrates the successive aspects of the organisation. The organisation’s internal factors depict that the organisation is getting recognised in different countries and can focus on the customers. Although in terms of achieving sustainability, the well-being of the employees is also to be considered. On that note, Boohoo PLC lacks the strategic vision to encompass the workforce towards productivity. As opined by Alshmemriet al. (2017), the theory of two factors proposed by Hertzberg can be implicated as it has been defined that motivation and hygiene are two factors that need to be fulfilled. The organisation’s strategic vision towards achieving sustainability is observable as the company has been focusing on reducing the impact on the environment through technological innovation. This helps in identifying the fact that Boohoo Plc. has been investing in the development of better customer experience and satisfaction. Therefore, the opportunity of the company to increase its market ownership is observable. However, the company’s threats involve high competition from premium brands such as ASOS, H&M, and the threat of legal compliances are also visible. Interpretation of the PESTLE can also be applied in this context to identify the threats. It can also be depicted that the company is making progress, and the application of web 3.0 can be opportunistic for developing a better customer experience for the company (Husain et al. 2020).

5. Conclusion

Making a complete evaluation of the report helps to identify that the financial performance of Boohoo PLC has decreased in terms of net profitability and liquidity; however, it has been observed that the business has been improving utilisation of its assets as the efficiency ratios increased in the last four years. This helps to gain insight that profitability and efficiency ratio has a reverse relationship, and it will be observed that when profits from sales decrease, then effective utilisation of assets is expected. Besides, the fashion retail industry contains several opportunities and threats for the company, and these are related to the political, economic, social, technological, environmental and legal aspects. The report also helps to conclude that Boohoo Plc has been able to expand its business globally, although the working culture in their supply chain is causing organisational weaknesses. Therefore, the business needs to develop strategic decisions in order to improve these aspects. Brexit has also impacted negatively as the cost of the products has increased for retailers for including high custom duties. However, increasing the investment in technology can also be a strategic approach for the company as it will allow them to achieve sustainability. For investors, the organisation can be considered profitable as earnings from each share have increased, and the e-commerce fashion retail market of the UK also has a positive future.

References

Alshmemri, M., Shahwan-Akl, L. and Maude, P., (2017). Herzberg’s two-factor theory. Life Science Journal, 14(5), pp.12-16. Retrieved from:https://www.lifesciencesite.com/lsj/life140517/03_32120lsj140517_12_16.pdf [Retrieved on: 1st October]

bbc.com, (2021). Retrieved from: https://www.bbc.com/future/article/20200310-sustainable-fashion-how-to-buy-clothes-good-for-the-climate [Retrieved on: 30th September]

boohooplc.com, (2021). Retrieved from: https://www.boohooplc.com/ [Retrieved on: 29th September]

boohooplc.com, (2021). Retrieved from: https://www.boohooplc.com/sites/boohoo-corp/files/all-documents/result-centre/2020/boohoo-com-plc-annual-report-2020-hyperlink.pdf [Retrieved on: 30th September]

Drury, C. (2018). Cost and management accounting. Cengage Learning. Retrieved from: https://www.academia.edu/download/61659347/StudentManual_-Drury_Q___A_Study_book_1_20200102-115374-1jy93px.pdf [Retrieved on: 1st October]

Dyson, J. R. (2020). Accounting for non-accounting students. Pearson Education. Retrieved from: http://digilib.umpalopo.ac.id:8080/jspui/bitstream/123456789/149/1/Accounting%20for%20Non-Accounting%20Students_Dyson.pdf [Retrieved on: 1st October]

esgclarity.com, (2021). Retrieved from:https://esgclarity.com/asi-divests-from-boohoo-in-response-to-slavery-investigation/ [Retrieved on: 30th September]

Goworek, H., Oxborrow, L., Claxton, S., McLaren, A., Cooper, T. & Hill, H., (2020). Managing sustainability in the fashion business: Challenges in product development for clothing longevity in the UK. Journal of Business Research, 117, 629-641. Retrieved from:http://irep.ntu.ac.uk/id/eprint/34228/1/11676_Oxborrow.pdf [Retrieved on: 30th September]

hostingdata.co.uk, (2021). Retrieved from:https://hostingdata.co.uk/online-shopping-statistics-uk/ [Retrieved on: 29th September]

Husain, T., Sani, A., Ardhiansyah, M. &Wiliani, N., (2020). Online Shop as an interactive media information society based on search engine optimization (SEO). International Journal of Computer Trends and Technology (IJCTT), 68(3), 53-57. Retrieved from:https://www.researchgate.net/profile/Asrul-Sani/publication/340298216_Online_Shop_as_an_interactive_media_information_society_based_on_

society-based-on-search-engine-optimization-SEO.pdf [Retrieved on: 1st October]

Idrees, S., Vignali, G. & Gill, S., (2020). Technological Advancement in Fashion Online Retailing: A Comparative Study of Pakistan and UK Fashion E-Commerce. International Journal of Economics and Management Engineering, 14(4), 318-333. Retrieved from: https://www.researchgate.net/profile/Sadia-Idrees-2/publication/341070063_Technological-Advancement-in-Fashion-Online-Retailing-A-Comparative-Study-of-Pakistan-and-UK-Fashion-E-Commerce_1/links/5eaba97b45851592d6ae7445/Technological-Advancement-in-Fashion-Online-Retailing-A-Comparative-Study-of-Pakistan-and-UK-Fashion-E-Commerce-1.pdf [Retrieved on: 29th September]

ionos.co.uk, (2021). Retrieved from:https://www.ionos.co.uk/digitalguide/websites/digital-law/data-protection-in-e-commerce/ [Retrieved on: 30th September]

Jung, J., Kim, S.J. & Kim, K.H., (2020). Sustainable marketing activities of traditional fashion market and brand loyalty. Journal of Business Research, 120, 294-301. Retrieved from:https://fardapaper.ir/mohavaha/uploads/2020/06/Fardapaper-Sustainable-marketing-activities-of-traditional-fashion-market-and-brand-loyalty.pdf [Retrieved on: 30th September]

McLaney, E. &Atrill, P., (2020). Accounting and Finance: An Introduction eBook PDF. Pearson Higher Ed. Retrieved from:https://books.google.com/books/about/Accounting_and_Finance_An_Introduction_e.html?id=FyzJDwAAQBAJ [Retrieved on: 1st October]

Nguyen, T.H.N., (2017). Integration of multi-channel distribution and its impact on profit of fast fashion companies. Retrieved from: https://aaltodoc.aalto.fi/bitstream/handle/123456789/26027/bachelor_Nguyen_Ngoc_2017.pdf?sequence=1 [Retrieved on: 30th September]

prolificnorth.co.uk, (2021). Retrieved from:https://www.prolificnorth.co.uk/news/digital/2018/07/boohoo-founders-invest-fashion-tech-platform [Retrieved on: 30th September]

Said, A.S., (2020). Essential Study in an Effort to Improve Satisfaction Tourism Travel. International Journal of Management (IJM), 11(2), 105-113. Retrieved from:https://www.academia.edu/download/62507944/IJM_11_02_01120200327-38645-16p8fxc.pdf [Retrieved on: 30th September]

statista.com, (2021). Retrieved from: https://www.statista.com/forecasts/480950/clothes-and-accessories-e-commerce-users-by-age-and-gender-digital-market-outlook-uk [Retrieved on: 30th September]

statista.com, (2021). Retrieved from:https://www.statista.com/statistics/794936/boohoo-plc-group-revenue-by-region/ [Retrieved on: 29th September]

statista.com, (2021). Retrieved from:https://www.statista.com/statistics/315506/online-retail-sales-in-the-united-kingdom/ [Retrieved on: 29th September]

Tag, M. & Country, B., (2021). ESG and Litigation: The Outlook for Shareholders and Listed Companies: Environmental, Social & Governance Law 2021. Renewable Energy, 17, p.09. Retrieved from:https://iclg.com/practice-areas/environmental-social-and-governance-law/4-esg-and-litigation-the-outlook-for-shareholders-and-listed-companies [Retrieved on: 30th September]

texprocil.org, (2021). Retrieved from:https://texprocil.org/ibtexnewsclipping/1625114407-IBTEX01072021.pdf [Retrieved on: 29th September]

Todd, P., (2017). E-commerce Law. Taylor & Francis. Retrieved from: https://books.google.com/books?hl=en&lr=&id=qhw3DwAAQBAJ&oi=fnd&pg=PT19&dq=UK+laws+for+ecommerce+businesses&ots=

8ymJFBfpEB&sig=fi4zkxNEYtW9LIEbLjBdRLp1v8E [Retrieved on: 29th September]

Watson, A., Alexander, B. &Salavati, L., (2018). The impact of experiential augmented reality applications on fashion purchase intention. International Journal of Retail & Distribution Management. Retrieved from: https://ualresearchonline.arts.ac.uk/id/eprint/14087/1/AMM_proof.pdf [Retrieved on: 29th September]