An evaluation of the efficient market hypothesis

1.Introduction

The efficient market hypothesis introduced by Fama (1970) suggests that at any given time share prices fully and fairly reflect all historical and newly available information. The theory is associated with the random walk model which implies that the future share price movements represent random deviations from past share prices. Therefore, the theory asserts that an investor could only obtain average market returns by share trading using all available information. The aim of this study is to ascertain the validity of the hypothesis by evaluating the evidence for and against the concept.

There are three forms of market efficiencies based on the efficient market model which depend on the strength of the availability of information.

In a weak-form efficient capital market, the current share prices are considered to only reflect all historical information such as past share price movements and trading history. The concept suggests that it is impossible for an investor to study past share price movements and predict the future share prices in order to outperform the market and consistently make abnormal gains.

Current share prices are considered to reflect all historical information and all publicly available information such as published company accounts, announcements, industry conditions, tax rates etc., in a semi-strong form efficient market and share prices are said to be able to react speedily and accurately in absorbing any new information as and when it becomes available, thus the knowledge of such information cannot be used to make abnormal gains.

Capital markets are considered to be strong-form efficient when security prices reflect all forms of historical and currently available information, which can be publicly available information as well as information which is not available publicly, including ‘insider information’. A market that is strong-form efficient makes it impossible for investors to make abnormal gains using any type of information whether it is publicly available or not. Moreover, most jurisdictions in many countries consider acting on ‘insider information’ a criminal offence and have imposed strict rules that help regulate this type of activity.

Even with strict legislation in place, capital markets do not seem to meet all of these criteria which is evident in some countries, since there have been occasions where investors have made profits acting on ‘insider information’ which have resulted in prosecutions against them.

2.Evidence for and against the efficient market hypothesis

In this section, the evidence for and against the efficient market hypothesis is critically evaluated in order to ascertain whether it is possible to exploit market inefficiencies to make above-average gains by trading in capital markets using all available information.

2.1 Evidence for weak-form efficiency

According to the Random walk model, it is argued that security prices are unpredictable, thus the knowledge of share prices of one time period cannot be used to predict the share prices of a future period. A study done by Kendall (1953) investigated the correlation between the price changes of securities at different points in time and found little correlation within a series of price movements in the stock market, supporting the random walk model. Fama (1965) performed a test run to evaluate the validity of the empirical random walk model, examined the length of the runs of successive price changes of the same sign and concluded that the direction of price changes were independent and the distribution of the direction was based on pure chance.

The filter tests technique is another way of trying to identify any significant long-term relationships in fluctuations of share prices by way of filtering out short-term price movements of shares. Alexander (1961) performed one of the earliest filter tests, and found that while filter tests may produce above-average returns in comparison to a simple buy and hold approach, when the transaction costs were taken into consideration it cancelled out the gains which again supports the weak-form efficient market model.

2.2 Evidence against weak-form efficiency

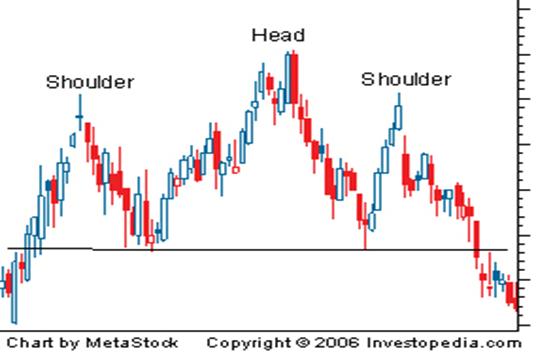

Despite the evidence that support the weak-form efficient market model, financial analysts argue that a technical analysis of past share prices can be used to establish a relationship between past and future share prices. The main technique of analysing historical data, termed ‘Chartism’, uses charts to perform a technical analysis in order to identify future trends of share prices using historical information such as past share price movements. One such trend is the ‘head and shoulders’ pattern where the chart formation resembles the upper part of a human body which is believed to be the most reliable trend-reversal pattern. There are many other trend patterns introduced by such analysts over the years; e.g., cup and handle, double top and double bottom etc. Furthermore, sophisticated computer software that promotes algorithmic trade has increased in popularity in recent times and is currently used by many in the stock market.

Chart formation of a ‘head and shoulders’ pattern

(source: www.investopedia.com)

According to a study by De Bondt and Thaler (1985), it was found that the portfolios of shares performing the worst over the last three to five years subsequently tend to out-perform the best-performing portfolios of the past periods i.e. prior ‘losers’ outperform prior ‘winners’, which suggests a strong returns reversal effect which is implied in a head and shoulders pattern. The study discovered substantial weak-form market inefficiencies.

Another study by Fama and French (1988) supports the return reversal concept, although it was argued that the autocorrelation in returns is weak in short holding periods (daily, weekly) and stronger in the long-horizon returns. Furthermore, the evidence of the research suggests that based on the negative autocorrelation of returns (return reversal) the predictability of returns of smaller firms is more in contrast to the predictability of returns of larger firms, hence linking predictability of returns to market capitalization.

The ‘Dow Theory’, which was developed over 100 years ago by Charles Dow, the first editor of the Wall Street Journal and co-founder of the Dow Jones Company, is a combination of trend analysis which challenges the efficient market paradigm (Arnold, 2008). The significance of the theory is that it still applies to current market indexes in the US. However, the amount of academic evidence that support the profitability of the theory is insufficient to fully appreciate the model.

Based on the evaluation of evidence provided in support of the theory such as the results of the serial correlation tests and filter tests, it can be argued that capital markets are at least weak-form efficient. The Chartists’ evidence against the theory does not seem to outweigh the rigorous studies that try to prove the existence of such a market. Although technical analysts may seem to be able to predict certain share price movements based on historical information of certain firms, the evidence demonstrates that predictability can be linked to market capitalization, i.e., predictability is stronger in smaller firms compared to larger firms. However, the smaller firms account only for a small proportion of the total equity traded in a capital market, thus reducing the economic significance. As for the ‘Dow Theory’ there is little academic support for the profitability of using the model.

2.3 Evidence for semi-strong form efficiency

The empirical research conducted by Fama et al. (1969, cited in Watson & Head, 2010) which examined the reaction of share prices to information announcements about share splits concluded that the market was efficient in absorbing the information to its share prices and as a result investors were unable to make abnormal gains using the information. Another empirical study that was conducted subsequently in relation to announcements of earnings (Ball and Brown, 1968) reached a similar conclusion supporting the semi-strong efficient market model.

A study by Franks et al. (1977) found that even though capital markets anticipated the possible benefits of mergers up to three months earlier than the actual announcement, it was still reflected in the share prices. This was the first published study to be based upon the London Business School database of monthly London Stock Exchange share prices.

2.4 Evidence against semi-strong form efficiency

Even with the strong evidence supporting the semi-strong form market efficiency, financial analysts challenge the model and perform fundamental analysis to estimate the real value of shares based on future returns. A comparison of this estimate and the market price is performed to establish an over or under valuation. Fundamental analysts argue that the market is less than perfectly efficient and use studies on market anomalies to fight their case. One such anomaly is the size of firms. It has been found that investing in small firms has produced greater returns in the long-run compared to larger firms. According to a study by Beechey et al. (2000, cited in Watson & Head, 2010) it was found that the above-average returns that were made by investing in smaller firms was the result of the greater risk associated with the investment, i.e., the higher the risk, the higher the return.

Another study used as an argument by the fundamental analysts is the ‘value investing’ concept, which suggests that investing in shares with low price/earnings ratios can produce abnormal gains. Research also shows that under-reaction or slow reaction of investors to certain types of information of certain circumstances may produce the possibility of abnormal returns. According to Bernard and Thompson (1989, cited in Arnold, 2008) it was found that cumulative abnormal returns (CARs) increased to good earnings announcements and decreased to bad earnings announcements even 60 days after the announcements.

Furthermore, there are investors who have not accepted the EMH concept and have made astonishing high returns consistently through investing and trading in the US stock market. Some of the names worth mentioning are Warren Buffet, regarded as the most successful investor in the world, who believes that market fluctuations can be used to one’s advantage, and John Neff, who advocates investing in shares with low price-earnings ratios i.e. ‘value investing’.

Despite a wealth of empirical studies that support the semi-strong efficient notion, the evidence does not seem to be strong enough to disregard the fact that the market can and has been outperformed by certain dedicated investors such as Warren Buffet and John Neff. Furthermore, since published research of the inefficiencies may result in the market reacting to eliminate the inefficiency, researchers that discover market inefficiencies may quietly use them to benefit from abnormal returns without publishing such studies. Moreover, a paradox that exists in this area is that for a market to be efficient it has to have many investors that believe it is inefficient.

2.5 Evidence for and against strong-form efficiency

Since ‘insider information’ is unknown, it is not possible to test the strong-form efficient market model; hence an indirect approach that examines how information provided by expert users perform in contrast to a measure such as the average return on the stock market needs to be employed to evaluate the theory. Fund managers can be viewed as experts that are in a strong position of making abnormal gains, although many studies have shown that this is not the case. Furthermore, an empirical study done by Keown and Pinkerton (1981) concluded that announcements regarding intended mergers through ‘insider information’ were incorporated to share prices rapidly which did not allow investors to make abnormal returns.

On the contrary, it can be argued that capital markets are not strong-form efficient due to the fact that certain individuals have access to market information before other investors and can make abnormal gains using this ‘insider information’. Although studies support a strong-form efficient market, there are quite a few prosecutions against investors for the offence of insider dealing, which suggests that the market can be exploited with such information. However, the number of court cases are said to be relatively few in contrast to the total transactions which take place in a capital market as a whole.

Based on the evidence, a definitive conclusion cannot be reached as to the existence of a strong-form efficient market simply because one could not know of such ‘insider information’ and how it might be quietly used to exploit the market. Indirect methods of testing the theory may not be practical. Individuals may have found ways to avoid exposing themselves whilst continuing to use insider information to gain high returns.

3.Conclusion

Based on the critical evaluation of the evidence for and against the efficient market hypothesis, as it stands, the theory cannot be accepted in its totality. Whilst the evidence tend to support the weak-form efficient market, inefficiencies may exist in the semi-strong market form which is evident in the massive stock portfolios that have been developed over the years by dedicated and skilful investors. Furthermore, the anomalies in share price behaviour cannot be disregarded, as it does challenge the efficient market model. The existence of a strong-form efficient market is highly unlikely and may be non-existent, simply because the illegal act of ‘insider dealing’ can be viewed as the most palpable one true method of making abnormal gains. It is probable that ‘insider information’ is still secretively used by investors to a certain extent to gain high returns without being exposed.

In conclusion, the evidence suggests that the market is generally efficient at least in a weak-form sense. Besides insider dealing, investors may outperform the market depending on their analytical proficiency, dedication and knowledge whilst for the majority of novice investors who lack these qualities the market should be treated as an efficient one, to avoid the losses on bad investment decisions.

- Arnold, G (2008). Corporate Financial Management. 4th ed. England: Prentice Hall.

- Ball, R. & Brown, P. (1968) An empirical evaluation of accounting income numbers. Journal of Accounting Research. Vol.6 (Issue: 2) p.159-178. EBSCOhost: Business Source Premier [Online]. Available at: http://search.ebscohost.com/login.aspx?direct=true&AuthType=ip,shib&db=buh&AN=6415708&site=ehost-live (Accessed on: 15th October 2011).

- De Bondt, W. F. M. & Thaler, R. (1985) Does the stock market overreact? The Journal of Finance [online], 40 (3), Available from: <http://time.dufe.edu.cn/jingjiwencong/waiwenziliao/20044291393677691.pdf> [Accessed on: 15th October 2011].

- Fama E.F., Fisher L., Jensen M.C., and Roll R. (1969) The Adjustment of Stock Prices to New Information. International Economic Review. 10 (Issue: 1) p.1-21.EBSCOhost: Business Source Premier [Online]. Available at: http://search.ebscohost.com/login.aspx?direct=true&AuthType=ip,shib&db=buh&AN=5711094&site=ehost-live (Accessed on: 15th October 2011).

- Fama, E. F. & French, K. R. (1988) Permanent and Temporary Components of Stock Prices. Journal of Political Economy, 96 (Issue), p.246. EBSCOhost: Business Source Premier [Online]. Available at: http://search.ebscohost.com/login.aspx?direct=true&AuthType=ip,shib&db=buh&AN=5199839&site=ehost-live (Accessed on: 15th October 2011).

- Fama, E. F. (1965) Random Walks in Stock Market Prices. Financial Analysts Journal, 21 (Issue: 5), p.55-59. EBSCOhost: Business Source Premier [Online]. Available at: http://search.ebscohost.com/login.aspx?direct=true&AuthType=ip,shib&db=buh&AN=7589211&site=ehost-live (Accessed on: 15th October 2011).

- Fama, E. F. (1970) Efficient capital markets: a review of theory and empirical work. Journal of Finance, 25 (Issue: 2), p.383-417. EBSCOhost: Business Source Premier [Online]. Available at: http://search.ebscohost.com/login.aspx?direct=true&AuthType=ip,shib&db=buh&AN=4660197&site=ehost-live (Accessed on: 13th October 2011).

- Franks, J. R., Broyles, J. E. & Hecht, M. J. (1977) An industry study of the profitability of mergers in the United Kingdom. Journal of Finance, 32 (Issue: 5), p.1513-1525. EBSCOhost: Business Source Premier [Online]. Available at: http://search.ebscohost.com/login.aspx?direct=true&AuthType=ip,shib&db=buh&AN=4657652&site=ehost-live (Accessed on: 16th October 2011).

- Kendall, M. G. (1953) The analysis of economic time series Part – I: Prices. Journal of the Royal Statistical Society, 116 (Issue: 1), p.11-34. JSTOR. [Online]. Available at: http://www.e-m-h.org/KeHi53.pdf (Accessed on: 15th October 2011).

- Keown, A. J. & Pinkerton, J. M. (1981) Merger Announcements and Insider Trading Activity: An Empirical Investigation. Journal of Finance, 36 (Issue: 4), p.855-869. EBSCOhost: Business Source Premier [Online]. Available at: http://search.ebscohost.com/login.aspx?direct=true&AuthType=ip,shib&db=buh&AN=4670685&site=ehost-live (Accessed on: 16th October 2011).

- Watson, D. & Head, A. (Eds.) (2010) Corporate Finance; Principles and Practise, (5th Ed.)Harlow: Pearson Education Ltd.