Critical Analysis of the Applications of the Balanced Scorecard

Number of words: 2586

Introduction

A Balanced Scorecard (BSC) refers to an organizational tool used by businesses to evaluate and regulate growth towards the attainment of established goals. Also, it is useful in communicating essential messages and aligning daily work performed by employees to strategy. This management system connects the organization’s mission and vision, the core values as well as focusing on the operations management, measures, and the targets of the organization. In the contemporary business world, managers are aware of how performance is influenced by measures but do not incorporate measures into their strategies[1]. For instance, operating systems and innovative strategies may be implemented to realize enhanced performance; still, managers continue to utilize the same financial indicators. Thus, they fail to introduce measures of monitoring processes and goals. BSC aims to align business processes to set strategies, visions, and missions, enhancing internal and external communications, and observing corporate performance alongside tactical objectives.

1.1.Problem Statement

In modern businesses, measuring performance is essential to monitor the effectiveness of business activities. BSC is a management tool designed to improve overall business performance. However, business still applies traditional measures that are financial in nature, neglecting non-financial performance indicators. Thus, such businesses fail to explore all possible performance threats which could affect organizational success and attainment of set goals.

1.2. Research Questions and Objective

This paper will address various research questions, including; how does BSC measures organizational performance? What are the implications of the BCS application? In addition, the objective of the paper will involve critically analysing how BSC can be applied to measure performance.

2. Application of Balanced Scorecard

2.1. How useful has BSC been?

BSC is vital for any senior management in organizations as it can be applied in process improvement in strategic planning as well as the development of superior strategies. Effective goal planning and subsequent evaluating and monitoring of established goals are crucial for organizational success. BSC thus plays a pivotal role in the regulation of essential elements of strategic management in businesses. The balanced scorecard is identified as a core element for senior organizational management and in the strategic mapping to visualize and relay the important message relating to the creation of values in any organization[2]. This process involves the demonstration of logic and efficient connection between the strategic objectives. Consequently, this leads to the improvement of services and the set goals as provided by the senior management capacity viewpoint, thus enabling the companies to perk up the internal strategies and consequently allow them to create desirable results that align with the organization’s expectations.

2.2. Popularity/Application/Adaptation

Upcoming management systems require to conform to demands and needs of company responsibility and also the shifting designs of managing human resources. The popularity of this system has reached as far as global reaching, and widely applied by the performance management system new generation. A survey on the application and popularity of the balanced scoreboard concluded that in 1200 large companies, 44% used outcome measurement systems, including the balanced scoreboard measurement system[3]. Initially, the purpose of this system was meant to address issues relating to organizational performance. Globally, over 70% of corporations have integrated BSC in their operations, and its implementation depends on its adaptation capacity and offers enhanced solutions that can substantially revolutionize the economy.

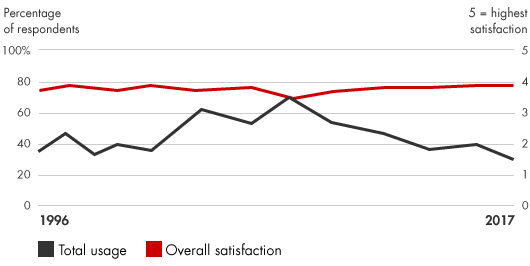

The adoption of the balanced scoreboard is demonstrated by the majority of senior management and other non-financial indicators for operational management through the economic vision as a management system. As evidenced, the adoption is depicted by a paradigm of the traditional systems that are applied in measuring the results of various problems[4]. The over-emphasis on financial indicators are not adequately integrated with another indicator hence making the adoption of the BSC method of multidimensional and incorporated support for senior management decision-making[5]. The theoretical fundamentals of the BSC adopt that the performance indicator is an essential management element. When improving high-level management processes, BSC provides the management with a superior understanding and better insight regarding their power and potential[6]. The implementation of this system by organizations globally deemed BSC a management tool that has the ability to describe and implement the developed goals. Founded on this strategy, the administrative function overseen by HR allows the objective setting to be functional and operational. The implementation of BSC thus allows operational control to be conducted efficiently. The figure below shows how BSC has been widely adopted by businesses. Although the total usage appears declining due to emergence of other models BSC overall satisfaction has significantly impacted businesses.

Figure 1: Showing BSC usage and satisfaction among selected businesses[7]. Source:(Bain.com, 2018)

The principal-agent designs established by economists involve the outputs that necessitate additional management actions that comprise the financial performance that evaluate budget implementation can be optimized. Operations and top-level management values that enhance trustworthy relations with stakeholders are essential in attaining corporate goals[8]. In addition, amounts spend by top-level management in increasing tangible assets value may have short-run in value creation. Expenditure growth thus is vital in generating future value that integrates economic measures of value-added. Furthermore, depending on dynamic programming, the optimum actions of conceptual model multi-period replicate on business period optimum actions[9]. Thus, the organizational management strives to exploit total goal attainment by heightening financial performance reported. Based on the conception model, the BSC identifies management limitations regarding financial goals in short-term episodes. Stakeholders that provide top-level management performance measurement with a multinational approach. Top-level management that utilizes performance management theory begins with the determination of objectives and interactions of different stakeholders’ approaches that describe the strategy that meets stakeholders’ expectations.

3. Critical Evaluation

The concept of BSC as applied in firms and organizations was developed by Robert S. Kaplan and David P. Norton in 1992 from the business review. This concept can be defined as a system that seeks to provide a balanced and all-inclusive framework for the judgment of the organizational performance from the viewpoint of financial or customer[10]. The perspectives given by the BSC are interrelated. For example, the primary objectives of the economic point of view are profitability. This is achieved through the achievement of the customer’s perspective and the goal of customer tastes and preferences. Furthermore, firms and organizations can meet the tastes and preferences of the customers through the internal critical process functions effectively[11]. Since the successes of the performance of internal critical processes depend on the organizational perception of learning and development. As such, the balanced scorecard balances the various aspects that give a comprehensive view of successful organizational functioning, in the aggressive environmental state of affairs.

The development of this system was based on finding developed from a study of corporate affairs. The finding assumed that even though the real assent played a significant role in the value creation in the business, organizations were not measuring or monitoring their assets in the management process[12]. As demonstrated, the primary reason for the application of this system in the corporate sector was to evaluate and assimilate intangible assets into an organization’s performance evaluation. However, despite its implementation the business management, the balanced scorecard has demonstrated a lack of concise purpose as differences have emerged in its interpretation and practice[13]. The definition of this method depends on the understanding of the organization, as many of them have formulated this system in need to support various strategic organizational goals. The particular group applies the BSC as a strategic evaluation technique that helps the decision-making process at the strategic management level. This follows the development of the worker’s incentive systems in the control stage. This is based on the need to improve the senior management of intellectual capital in the performance measure.

3.1. Benefits of Balanced Scorecard

BSC has multiple benefits when applied as a management tool by senior management. Considering different elements of organizational performance, BSC enables organizations to acquire a balanced perception of organization performance[14]. Unlike traditional techniques of managing systems, BSC provides top-level management with a better view with goals progress and scientific management. Individuals may appear performing well in financial terms, but in the real sense, their customer satisfaction may be below average, or employee education may be down. BSC steps in to provide management with insights on how affairs of the organization are managed[15]. In addition, BSC assists organizations in bridging the gap between organizational goals, mission statement, and how day-to-day operations support corporate vision and mission. Applying BSC strategy in companies is useful in evaluating the immediate future. Besides, organizations can address their long-term plans or financial bottom line. Thus, BSC enables the management to establish short, medium, and long-term goals effectively and within a short period.

3.2. Limitations of Balanced Scorecard

Despite the wide-ranging advantage of this idea, the balanced scorecard has its share of the drawbacks. For instance, the BSC performance is subjective. Unlike another advanced system that measures the organization’s performance system, the BSC does not quantify as a management option. The training of employees, as provided by this system, is mandated to a particular number of hours in meeting the organization’s innovation share[16]. The level of demand by the personnel can be daunting to the employers. The setting of goals with the high morale of workers with the lay saves the money to be counterproductive methods.

Moreover, the balanced scorecard improves the reporting without improving the commercial quality, which is viewed as an additional set of a reporting system that distracts the achievement of the real objectives. Additionally, this system does not comprise the direct financial scrutiny of economic or organizational risk management. This implies that the system does not contain the opportunities that include the opportunity cost calculations.

4. Conclusion and Outlook

Based on the definition, the BSC is depicted as part of a description of senior management rules that incorporates various designs and plans that involved in the business amendment. BSC, as demonstrated from the analysis, is critical in positioning the management tools in any company. The principles of the management are still present in the contemporary business calling for more formal rules of success for the companies. This assumption is useful in positioning the most important tools. BSC is designed to solve organization performance issues, and its implementation into business planning and operational goals must be outright succinct and comprising measures relating to organizational performance. Understanding BSC assists management in transcending thoughts regarding functional barriers and ultimately result in improved problem-solving and decision-making. BSC keeps organizations looing and moving forwards rather than backward.

5. Bibliography

Asgari, Nasrin, and Soroush Avakh Darestani. “Application of multi-criteria decision making methods for balanced scorecard: a literature review investigation.” International Journal of Services and Operations Management 27, no. 2 (2017): 262-283.

Awadallah, Emad A., and Amir Allam. “A critique of the balanced scorecard as a performance measurement tool.” International Journal of Business and Social Science 6, no. 7 (2015): 91-99.

Bain. 2018. Balanced Scorecard. [online] Available at: <https://www.bain.com/insights/management-tools-balanced-scorecard/> [Accessed 22 May 2020].

Gleich, Ronald, and Diane Robers. “Umsetzung und Controlling einer Kommunikationsstrategie mit der Balanced Scorecard.” In Handbuch Controlling der Kommunikation, pp. 139-162. Springer Gabler, Wiesbaden, 2016.

Gollner, Juergen Alexander, and Ilona Baumane-Vitolina. “Measurement of ERP-project success: Findings from Germany and Austria.” Engineering Economics 27, no. 5 (2016): 498-508.

Hohensee, Patrick. Einsatzmöglichkeiten und-grenzen der Balanced Scorecard im Konsumgütermarkt. Eine kritische Analyse. GRIN Verlag, 2015.

Jossé, Germann. Balanced scorecard: Ziele und Strategien messbar umsetzen. Vol. 50961. CH Beck, 2018.

Kohlstock, Barbara. “Eine kritische Analyse.” Ambivalenzen des Ökonomischen: Analysen zur „Neuen Steuerung “im Bildungssystem 29 (2015): 143.

Terziev, Venelin, Banabakova Vanya Kuzdova, Oleg Latyshev, and Marin Georgiev. “Opportunities of application of the balanced scorecard in management and control.” Proceedings of ADVED (2017): 9-11.

Zelewski, Stephan, Dieter Ahlert, Peter Kenning, and Reinhard Schütte, eds. Wissensmanagement in Dienstleistungsnetzwerken: Wissenstransfer fördern mit der Relationship Management Balanced Scorecard. Springer-Verlag, 2015.

[1] Kohlstock, Barbara. “Eine kritische Analyse.” Ambivalenzen des Ökonomischen: Analysen zur „Neuen Steuerung “im Bildungssystem 29 (2015): 143.

[2] Hohensee, Patrick. Einsatzmöglichkeiten und-grenzen der Balanced Scorecard im Konsumgütermarkt. Eine kritische Analyse. GRIN Verlag, 2015.

[3] Gollner, Juergen Alexander, and Ilona Baumane-Vitolina. “Measurement of ERP-project success: Findings from Germany and Austria.” Engineering Economics 27, no. 5 (2016): 498-508.

[4] Gollner, Juergen Alexander, and Ilona Baumane-Vitolina. “Measurement of ERP-project success: Findings from Germany and Austria.” Engineering Economics 27, no. 5 (2016): 498-508.

[5] Gleich, Ronald, and Diane Robers. “Umsetzung und Controlling einer Kommunikationsstrategie mit der Balanced Scorecard.” In Handbuch Controlling der Kommunikation, pp. 139-162. Springer Gabler, Wiesbaden, 2016.

[6] Terziev, Venelin, Banabakova Vanya Kuzdova, Oleg Latyshev, and Marin Georgiev. “Opportunities of application of the balanced scorecard in management and control.” Proceedings of ADVED (2017): 9-11.

[7] Bain. 2018. Balanced Scorecard. [online] Available at: <https://www.bain.com/insights/management-tools-balanced-scorecard/> [Accessed 22 May 2020].

[8] Gleich, Ronald, and Diane Robers. “Umsetzung und Controlling einer Kommunikationsstrategie mit der Balanced Scorecard.” In Handbuch Controlling der Kommunikation, pp. 139-162. Springer Gabler, Wiesbaden, 2016.

[9] Terziev, Venelin, Banabakova Vanya Kuzdova, Oleg Latyshev, and Marin Georgiev. “Opportunities of application of the balanced scorecard in management and control.” Proceedings of ADVED (2017): 9-11.

[10] Jossé, Germann. Balanced scorecard: Ziele und Strategien messbar umsetzen. Vol. 50961. CH Beck, 2018.

[11] Awadallah, Emad A., and Amir Allam. “A critique of the balanced scorecard as a performance measurement tool.” International Journal of Business and Social Science 6, no. 7 (2015): 91-99.

[12] Zelewski, Stephan, Dieter Ahlert, Peter Kenning, and Reinhard Schütte, eds. Wissensmanagement in Dienstleistungsnetzwerken: Wissenstransfer fördern mit der Relationship Management Balanced Scorecard. Springer-Verlag, 2015.

[13] Awadallah, Emad A., and Amir Allam. “A critique of the balanced scorecard as a performance measurement tool.” International Journal of Business and Social Science 6, no. 7 (2015): 91-99.

[14] Zelewski, Stephan, Dieter Ahlert, Peter Kenning, and Reinhard Schütte, eds. Wissensmanagement in Dienstleistungsnetzwerken: Wissenstransfer fördern mit der Relationship Management Balanced Scorecard. Springer-Verlag, 2015.

[15]Asgari, Nasrin, and Soroush Avakh Darestani. “Application of multi-criteria decision making methods for balanced scorecard: a literature review investigation.” International Journal of Services and Operations Management 27, no. 2 (2017): 262-283.

[16] Asgari, Nasrin, and Soroush Avakh Darestani. “Application of multi-criteria decision making methods for balanced scorecard: a literature review investigation.” International Journal of Services and Operations Management 27, no. 2 (2017): 262-283.