Business Case for Corporate Social Responsibility

Number of words: 3624

Executive Summary

One of the trending topics in today’s corporate world is ‘Corporate Social Responsibility, popularly known by its abbreviations, ‘CSR.’ The corporate sector and the society are interdependent. It is expected that the corporate world should work like a honeybee, the honeybee that collects honey from the flower without harming it and provides the honey for the welfare of society. The evidence in the business history emphasizes that the business’s growth and development are dependent on society; if society thrives, then businesses grow; on the other hand, the business fails when society rejects it. No business in the world thrives without the approval of society. This report is an effort to analyse the different responsibilities of CSR, such as economic, legal, ethical, and philanthropical responsibilities. The report also illustrates different stakeholders of CSR. A brief discussion of the benefits of CSR is carried out along with real-life examples where the importance of CSR is mistreated.

Keywords: CSR, Corporate, Society, economic, legal, ethical, philanthropical.

Contents

| Executive Summary | 2 |

| 1.0 Introduction | 4 |

| 2.0 Literature review | 5 |

| 3.0 Analysis and discussion | 7 |

| 3.1 CSR responsibilities | 7 |

| 3.1.1 Economic responsibilities | 8 |

| 3.1.2 Legal responsibilities | 9 |

| 3.1.3 Ethical responsibilities | 9 |

| 3.1.4 Philanthropic responsibilities | 10 |

| 3.2 Stakeholders | 10 |

| 3.2.1 Shareholders | 11 |

| 3.2.2 Employees | 11 |

| 3.2.3 Customers | 12 |

| 3.3 Benefits of CSR | 12 |

| 3.4 The case of the British Petroleum spill in the Gulf of Mexico | 12 |

| 4.0 Conclusion | 13 |

| References | 14 |

1.0 Introduction

The idea of Corporate Social Responsibility has gathered worldwide attention and debates due to its growing importance in the global economy. The complexity of the business has increased due to globalization and increased trade. The growing complexity requires more transparent and open business practices built on ethical values, respect towards society, personnel, stakeholders, and the environment. Corporate Social Responsibility is a tool to deliver sustainable values to society. According to Bowen (1953), CSR is the operational tool for businesses to exceed society’s expectations through ethical, legal, economic responsibilities. According to World Business Council for Sustainable Development, the definition of CSR is “the commitment of business to contribute to sustainable economic development, working with employees, their families and the local communities’’ (WBCSD, 2001). Therefore, the principle of CSR emphasizes the responsibilities of a business corporation to fulfil the commitment of a society (Weber, M. 2008; Rigoberto, J. 2009).

2.0 Literature review

The roots of Corporate Social Responsibility go beyond world war II. However, the discussion of the history in this report will be restricted to the post-war era. Especially 1945 to 1960, during the early years of the cold war. Many business scholars in the United States advocated CSR to defend the “free-market capitalism” against the Soviet Union (Spector, B. 2008). The limited disclosure about CSR was presented in the year 1950. However, a former executive of a Standard oil company in New Jersey, Mr. Frank Abrar, expressed concerns over the extended responsibilities in the complex society (Abrams, F. 1951). The influential book “Social Responsibilities of the Businessman” by Howard Bowen was published in 1953 (Bowen, H. 1953); the book was ahead of its time. Another contributor to CSR literature, William Frederick, had proposed three core ideas about CSR, which stands out to be exceptional in the 1950s.

The idea includes, “manager to be a public trustee, the balancing of competing claims to corporate resources, and corporate philanthropy” (Frederick, W. 2008). The decade of the 1950s experienced limited discussion regarding linking business benefits with CSR. The main focus of CSR was to do good work for society and the relevant responsibilities of the businesses, but Theodore Levitt gave the warning to the business world in the 1950s regarding risks of social responsibility (Levitt, T. 1958). Despite the warning given by Levitt, the popularity of CSR increased and took shape during the 1960s. The formal definition of CSR was introduced in the late 1970s. All the emphasis on the definition was on the corporate social responsibility performance (CSP) (Sethi, S. 1975). The companies were not only pretending to assume the responsibilities, but they were responding to the theory of corporate social environment (Ackerman, R. 1973; Murray, E. 1976). The distinction between corporate social responsibility and responsiveness was formalized by Frederick (1978) as CSR-1 and CSR-2. Social responsibility posture was assumed by the companies that emphasised CSR-1, whereas the responsive posture or responding to the society in actuality was adopted by the companies emphasised on CSR-2. On the other hand, CSP was an effort to merge CSR-1 and CSR-2 to achieve results in the initiatives related to social responsibilities. The emphasis on the CSP emerged during the 1970s (Carroll, A. 1979; Wartick et al., 1985; Wood, M. 1991).

The idea of the business case emerged due to the focus on CSR. Therefore, it was anticipated that when the outcome of the business cases is emphasised, it would be easier to measure the results of CSR practices and policies. 1980s decade shows the minimum attention in the literature contribution in terms of definitions and perception of CSR; however, alternative themes concerning CSR concepts emerged that improved the popularity of CSR. Some of the variants of the new CSR concepts include stakeholder management, corporate ethics, public policy, and the development of the CSP, introduced in 1970 (Carroll, A. 1999). According to Fredrick (2008), the phase of business ethics started in the 1980s, and the focus was on developing ethical corporate culture (Frederick, W. 2008). The research to find the link between corporate financial performance and CSR has increased during the 1980s (Lee, M. 2008P). Therefore, the academic research for the business case for CSR has grown during the 1980s. This trend of CSR continued till the late 1990s, and the efforts to push CSR to global business have increased in this decade. The era of global citizenship represented by the 1990s and 2000s (Fredrick, W. 2008). However, the early 2000s have experienced various scandals, such as Enron, which was soon followed by wall street scandals in 2008, severely affecting the global economy (Carroll, A. 2009). The quest of CSR to find business rightfulness and its obsession with business ethics hampered the continuous growth and development of CSR in the entire world, but some significant developments were made in continental Europe and the United Kingdom (Moon, J. 2005). The pursuit for the CSR business case undoubtedly becomes a leading theme during this time, exclusively due to the business community striving to legalize their activities, and it is still ongoing. The concept of sustainability and sustainable development became a point of interest for the business community in the early 2000s, and eventually, the theme of sustainability became the essential theme of CSR.

3.0 Analysis and discussion

3.1 CSR responsibilities

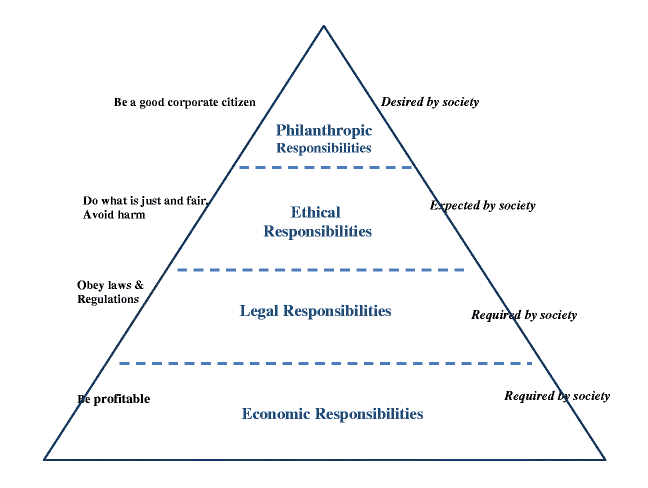

It is suggested that the framework of the corporate responsibilities should be in a way that everyone in the company should be included so that it can be readily accepted by the cautious professional. There are four critical responsibilities in CSR, primarily ethical, legal, economic, and philanthropical. These four responsibilities of CSR are regarded as categories and illustrated in the form of a pyramid, as shown in figure 1. (Carroll, A. 1991). Theoretically, it is always required that all of these responsibilities exist in the CSR framework to some extent. However, it has been observed that ethical and philanthropical responsibilities have taken considerable place in the CSR framework in recent years.

Figure 1: Carroll’s Pyramid of CSR (Carroll, A. 1991)

As discussed in the literature review, CSR was defined in the year 1979 in four parts. Whereas the pyramid shown in figure 1 was the extraction of the four-part definition by Carroll in 1991. The pyramid aimed to emphasize the building-block nature of the CSR framework rather than its definition aspect. The geometric design of the pyramid was selected due to its simplicity, spontaneous, and built to survive the time test. Accordingly, the pyramid base has economic responsibility as it is the first prerequisite of any business. Similar to the foundation of a building which must be strong enough to support the entire organization and the strong, sustainable profitability required to fulfil other expectations from the society from the business. The essence of the economic responsibility at the base of the CSR pyramid depicts strong economic and sustainable organization.

Similarly, it is expected that businesses should obey and comply with the rules and regulations. Furthermore, ethics are the values of the society, which are usually in non-written format, which means businesses are expected to work on the right and fair path to minimize the harm to the people involved and the environment. Finally, philanthropical responsibilities are placed higher at the apex of the pyramid as society expects businesses to be good corporate citizens and provide financial, physical, and human resources to society. In a nutshell, the pyramid’s design reflects the fundamental roles of the businesses and the expectation of the society (Carroll, A. 1991).

3.1.1 Economic responsibilities

The primary existence of any business depends on the economic condition; in addition, the businesses have specific economic responsibilities towards the society that allows them to be developed in a sustained matter. Therefore, an organization must be profitable and motivate stakeholders to invest in the business to keep resources running the operation. In its primary operation, businesses, sales goods, or services required by society. Society then purchases these goods and services according to their need which provides profits to the businesses—the profits created due to value addition which benefits all the company’s shareholders. For business growth, profits are necessary and provide rewards/incentives to the shareholders. When the profits are reinvested, then the business grows (Carroll, A. 2016).

3.1.2 Legal responsibilities

Along with the economic responsibilities, the businesses must follow legal compliance expected by the society for business to function. Legal compliance includes laws and regulations known as “codified ethics” of the society established by federal lawmakers, state, and local authorities. Due to these legal compliances, the position of a compliance officer is regarded as most important in the organizational structure. Following are the significant expectations from the businesses while meeting these legal responsibilities (Carroll, 2016),

- The performance should follow the laws of government and the authority

- It is expected for the businesses to comply with local, state, and federal regulation

- Businesses should conduct themselves as “law-abiding corporate citizens” (Carroll, 2016)

- The business should fulfil all the legal obligations towards the community

- Complying with all the minimal legal requirements while providing the goods and services

3.1.3 Ethical responsibilities

Ethical responsibilities, however, are not codified into the law, but they prohibit a member of society from indulging in the wrong activities. Ethical norms surround the economic as well as legal responsibilities. Ethical responsibilities are those expectations that echo a fair attitude towards shareholders, employees, consumers, and society. Following are the essential expectations of the business (Trong Tuan, 2012),

- While performing, the business should consistently fulfil expectations of social values as well as ethical norms

- It is required that businesses should recognize and respect the moral and ethical norms accepted by the society

- The management should avoid compromising on the ethical values of society to accomplish business goals

- Good corporate citizen means having ethical and moral values

- More than legal compliance, it is necessary for an organization to recognize ethical behaviour and business integrity (Carroll, 1991)

3.1.4 Philanthropic responsibilities

Business philanthropy consists of all forms of business charities. Voluntary and discretionary activities of the businesses are included in corporate philanthropy. The philanthropic responsibilities are also regarded as businesses following society’s expectations to become excellent corporate citizens. Various human welfare programs are examples of Philanthropical responsibilities. In addition, a financial contribution towards community, societies, and education are included in the philanthropical responsibilities.

3.2 Stakeholders

There are many elements of society involved in business activities. Also, corporations are keen to involve the shareholders in the decision-making activities that address social challenges in front of the organization as the shareholders are aware of the significance of business decisions on society and the environment. Shareholders can punish or reward corporations accordingly. Therefore, the business case of CSR required identifying different stakeholders that may directly affect the functioning of the businesses, or they may affect the business functions. Different interest groups are associated with the corporates: investors, employees, customers, suppliers, creditors, government, and society. However, for this report, the discussion is limited to the three key stakeholders: investors/shareholders, employees, and customers (Trong Tuan, 2012).

3.2.1 Shareholders

The primary responsibility of any business management is to secure the interest of the shareholders (Trong Tuan, 2012). Although the interest of both major and minor shareholders can be protected by involving them in the decision-making process, especially for the major shareholders, minor shareholders should be regularly informed about the organization’s functions. Therefore, corporate management is accountable for safeguarding the money invested by various shareholders.

3.2.2 Employees

One of the direct interest groups of a business organization is employees. Therefore, the businesses have the liability to satisfy their basic needs, and thus it is evident for the management to protect the worker’s interest. Following ways could be adapted to protect the interests of the employees (Trong Tuan, 2012),

- Management should treat employees with respect and regard them as another wheel of the vehicle

- The process developed by the management should promote cooperation between the management and employee

- Management should consider and adopt a progressive labour policy aligned with the union rights of the workers. The management should involve the management of workers in outlining labour policy

- The wages paid to the workers should be reasonable and fair along with other

3.2.3 Customers

The companies are running efficiently for the customers; therefore, corporate management owes a great deal to the end-users of their goods or services. The interests of the customers can be protected by the following methods (Trong Tuan, 2012),

- The price charged to the customer for the goods or services should be reasonable

- The quality and the standards for the goods and the services should be uniform

- Management should stay away from fraudulent practices such as hoarding or creating false scarcity

- Management should restrain themselves by creating misleading advertisements

3.3 Benefits of CSR

There are various benefits the CSR activity offers to the businesses, which are briefly pointed out below,

- The CSR activity helps to reduce cost and associated risk

- The CSR helps the business to build its brand across the society, which helps them gain a competitive advantage

- Corporate philanthropy, its corresponding responsibility, and transparency in the business develop the legitimacy and the reputation of the business

- Stakeholder engagement in the CSR decisions and the charities helps to create a win-win situation along with value creation

3.4 The case of the British Petroleum spill in the Gulf of Mexico

British Petroleum was regarded as one of the best sustainable implementing programs before the Deepwater Horizon accident. BP has maintained an “A+” for a considerable period for the Global Reporting Initiatives known as GRI. The BP has achieved several recognitions and awards for sustainability which is an integral part of CSR. However, Deepwater Horizon’s incident created a question of the difference between the perception and the reality of the CSR industry (Cort, T. 2010). During the investigation, it has been found that the suppliers of the BP were putting minimal efforts towards health and safety; however, the report furnished by BP shows robust health and safety measures for the worldwide operations. Likewise, inappropriate relationships of BP with the US minerals management service were exposed, which was against the code of conduct elaborated in the company’s CSR policy. (Cort, T. 2010) In a nutshell, BP has diverted its focus from its CSR policies intentionally or unintentionally, which has caused havoc in the Gulf of Mexico and damaged the company image severely.

4.0 Conclusion

The report discusses the history and evolution of CSR along with various responsibilities of the organization concerning CSR. The key stakeholders have been discussed concerning protecting their interests and the method for the same. Various benefits that CSR can offer to businesses have been discussed. The case of the British Petroleum disaster has been discussed briefly, and it has been understood that one of the main reasons for disaster is a deviation from CSR policies such as ethics and sustainability. CSR can help the companies and the communities; however, the deviation can cause unimaginable damage. Along with various benefits of CSR to businesses, the activity of CSR benefits society at large.

References

Abrams, F. (1951). Management’s responsibilities in a complex world. Harvard Business Review, pp.29-34.

Ackerman, R. (1973). How companies respond to social demands. Harvard Business Review, July/August 88–98.

Bowen, H. (1953). Social Responsibilities of the Businessman. New York: Harper.

Carroll, A. (1999). Corporate social responsibility: evolution of a definitional construct. 38th ed. Business and society, pp.268-295.

Carroll, A. (2016). Carroll’s pyramid of CSR: taking another look. International Journal of Corporate Social Responsibility, 1(1).

Carroll, A. B. (1991). The pyramid of corporate social responsibility: toward the moral management of organizational stakeholders. Business Horizons, 34(4), 39–48.

Carroll, A.B. (1979). A three-dimensional conceptual model of corporate social performance. Academy of Management Review, 4, pp. 497–505.

Carroll, A.B. (2009). A look at the future of business ethics. Athens Banner-Herald

Cort, T. (2010). Lessons for the CSR Industry from the Deepwater Horizon Spill. [online] GreenBiz. Available at: https://www.greenbiz.com/blog/2010/07/27/lessons-for-csr-reporting-from-deepwater-horizon-spill [Accessed 2 Dec. 2018].

Frederick, W.C. (1978). From CSR1 to CSR2: the maturing of business and society thought. Working Paper 279, Graduate School of Business, University of Pittsburgh.

Frederick, W.C. (2008). Corporate social responsibility: deep roots, flourishing growth, promising future. In Crane, A., McWilliams, A., Matten, D., Moon, J. and Siegel, D. (eds), The Oxford Handbook of Corporate Social Responsibility. Oxford: Oxford University Press, pp. 522–531.

Lee, M.P. (2008). A review of the theories of corporate social responsibility: its evolutionary path and the road ahead. International Journal of Management Reviews, 10, pp. 53–73.

Levitt, T. (2018). The dangers of social responsibility. September–October: Harvard Business Review, pp.41-50.

Mahmoud, M., Blankson, C. and Hinson, R. (2017). Market orientation and corporate social responsibility: towards an integrated conceptual framework. International Journal of Corporate Social Responsibility, 2(1).

Moon, J. (2005). An explicit model of business-society relations. In Habisch, A., Jonker, J., Wegner, M., and Schmid- peter, R., Corporate Social Responsibility Across Europe. Berlin: Springer, pp. 51–65.

Murray, E. (1976). The Social Response Process in Commercial Banks: An Empirical Investigation. Academy of Management Review, 1(3), pp.5-15.

Rigoberto Parada Daza, J. (2009). A valuation model for corporate social responsibility. Social Responsibility Journal, 5(3), pp.284-299.

Sethi, S. (1975). Dimensions of Corporate Social Performance: An Analytical Framework. California Management Review, 17(3), pp.58-64.

Spector, B. (2008). “Business Responsibilities in a Divided World”: The Cold War Roots of the Corporate Social Responsibility Movement. Enterprise and society, 9(2), pp.314-336.

Trong Tuan, L. (2012). Corporate social responsibility, ethics, and corporate governance. Social Responsibility Journal, 8(4), pp.547-560.

Wartick, S.L., and Cochran, P.L. (1985). The evolution of the corporate social performance model. Academy of Management Review, 10, pp. 765–766.

Weber, M. (2008). The business case for corporate social responsibility: A company-level measurement approach for CSR. European Management Journal, 26(4), pp.247-261.

Wood, DJ (1991). Corporate social performance revisited. Academy of Management Review, October, pp. 691–718.